| Analysis of large-scale energy storage business model |

| Release time:2022-12-27 09:28:51| Viewed: |

Analysis of large-scale energy storage business model

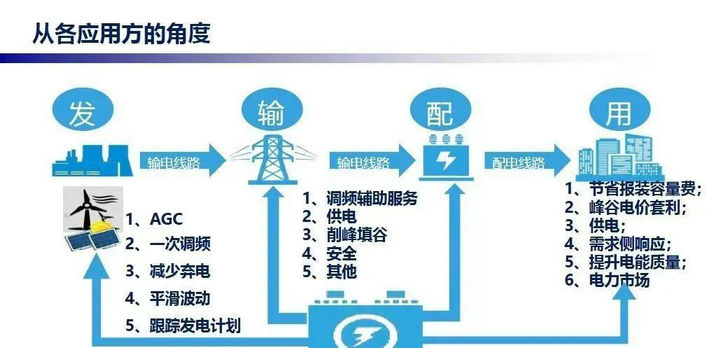

The development of the energy storage industry is driven by both the market and the policy, and the main body is determined by the energy storage investors and policy makers. The policy makers consider the energy transformation and the construction of new power systems, and actively promote the development of the energy storage market. The energy storage investors are most concerned about the economic benefits of energy storage. At present, the application scenarios of large-scale energy storage in China are mainly wind power distribution and storage, frequency modulation and other auxiliary services, independent shared energy storage, and industrial and commercial energy storage.

Wind and solar energy allocation and storage: new energy cost under the pressure of policy allocation

The overall pressure on new energy consumption across the country has improved. At the beginning of the "Twelfth Five Year Plan", the national new energy consumption pressure was high, and the overall wind and light abandonment rate was high, of which the wind abandonment rate reached 19% in 201. Later, China paid attention to the construction of new power systems, solved the new energy consumption capacity, and the wind and light abandonment rate was significantly improved.

The pressure of new energy consumption shows a trend of regional differentiation. In terms of specific sub regions, North China, Northwest China and Northeast China have sufficient scenery resources and are the main construction areas for large-scale centralized scenery projects. According to the data of the National New Energy Consumption Monitoring Center, the wind and light abandonment in 2021 will be mainly concentrated in these three regions, with wind abandonment rates of 1.9%, 5.8% and 0.9% respectively in North China, Northwest China and Northeast China, and light abandonment rates of 6.2%, 5.2% and 2.9% respectively.

The proportion of scenery allocation and storage varies from region to region, and the range is generally 10-20%. Nationwide, the allocation and storage of scenery projects has basically become a hard target, and the allocation and storage ratio is generally 10% - 20% of the installed capacity of new energy projects; By region, some regions in Northeast China, North China, Central China and Northwest China have a relatively high proportion of photovoltaic storage, while the proportion of photovoltaic storage in Inner Mongolia is required to be 20-30%. The greater the pressure of new energy consumption, the faster the new energy installation speed is promoted, and the higher the allocation and storage ratio. For example, Shandong Zaozhuang is the only city in Shandong Province that has all its districts and cities included in the whole county roof distributed photovoltaic development pilot, and the allocation and storage ratio is as high as 15-30%.

The proportion of new energy under policy pressure will increase, and the proportion of allocated reserves is expected to increase. New energy projects have strong policy pressure. China attaches great importance to the consumption of new energy, and will circulate a notice of criticism for provinces that fail to complete the responsibility weight of new energy power generation consumption. According to the notification of the National Energy Administration on the completion of the responsibility weight of renewable energy electricity consumption in 2021, some regions, such as Xinjiang, Gansu and other provinces, were criticized in the notification because they failed to meet the targets. The installation of new energy continues to increase, and it is more difficult to smooth the fluctuation of new energy power. Therefore, in the future, the installation of new energy will continue to increase, and the proportion of allocation and storage will also develop towards large capacity. The policy pressure superimposes on the increase of new energy installation, and the proportion of new energy allocation and storage in each province is expected to increase.

The revenue from wind and solar energy allocation and storage comes from improving the consumption rate and increasing the revenue from grid connection of power generation. As far as the investors of new energy projects are concerned, the revenue from strong wind power allocation and storage mainly comes from improving the consumption rate, which is equivalent to increasing the utilization hours. In most regions, the wind power consumption rate is more than 90%, so the consumption rate of allocation and storage is not increased significantly.

We separately calculate the economy of wind power/photovoltaic projects with or without energy storage.

The core assumptions of wind power and distribution and storage are as follows:

1. The installed capacity is 200MW, and the annual utilization hours are 2300 hours;

The core assumptions of photovoltaic and storage are as follows:

1. The installed capacity is 50MW, and the annual utilization hours are 1300 hours;

The allocation and storage of scenery is a cost item of the scenery project, which lowers the overall internal rate of return by about 1 1pct. The revenue model of wind power distribution and storage is single, and the grid price is relatively low, so there is no economy in distribution and storage. The internal rate of return of wind power projects without energy storage is 9.5%, and that of photovoltaic projects is 6.2%; Under the condition of self built 10% energy storage, the internal rate of return of wind power projects will decrease by 1.3 pct and that of photovoltaic projects will decrease by 1.4 pct. Assuming that other conditions remain unchanged, the cost of energy storage needs to be reduced to less than 0.75 yuan/Wh to bring benefits to the Wind Park project.

Economically driven wind and solar energy distribution and storage projects drive down costs and greatly reduce energy storage performance. For investors of new energy projects, the maximization of economy is to minimize the cost of energy storage projects. From the energy storage and energy storage projects tracked by the electricity market in October 2022, the bid winning price of new energy distribution and storage is lower than that of other enterprises. The weighted average quotation of new energy distribution and storage projects is 1.43 yuan/Wh, while the weighted average quotation of independent energy storage and user side energy storage is 1.88 yuan/Wh and 2.07 yuan/Wh respectively. The cost of new energy distribution and storage is controlled. The purchased equipment and cells are worse than other scenarios in terms of energy storage, so the energy storage performance is greatly discounted. According to the data in the Research Report on the Operation of New Energy Distribution and Storage, under the pressure of high cost, some projects have selected energy storage products with poor performance and low investment cost, increasing the potential safety hazards. From January to August 2022, the number of unplanned shutdowns of the national electrochemical energy storage project reached 329.

Sharing energy storage has become a compromise scheme for new energy distribution and storage. Shared energy storage is a large-scale independent energy storage project built by a third-party investor. The investor of a new energy project can meet the policy requirements by leasing part of the capacity of independent energy storage, and pay a certain lease fee for independent energy storage every year. For investors of new energy projects, the capacity lease fee is paid annually, reducing the huge cash flow pressure of initial investment; For investors of shared energy storage, independent energy storage power stations have more income models and higher return on investment. Therefore, the mode of leasing and sharing energy storage has become a trend for new energy projects to meet the requirements of policy allocation.

The cost pressure of shared energy storage for new energy leasing is reduced, and the demand for shared energy storage is expected to increase rapidly. We calculate the internal rate of return of new energy leasing and shared energy storage. The parameters of wind power photovoltaic project remain unchanged, and the lease expense is assumed to be 300 yuan/KW * year. When the allocation and storage ratio is 10%, the IRR of wind power projects decreases by 0.1 pct (self built energy storage decreases by 1.2 pct), the IRR of photovoltaic projects decreases by 0.9 pct (self built energy storage decreases by 1.1 pct), and the cost pressure of wind power projects decreases. The scale of wind power installation is large, and the amount of investment is large. Shared energy storage can effectively reduce the cash flow pressure and cost pressure caused by the initial investment. Therefore, the income increases significantly, and the demand for shared energy storage is expected to rise rapidly.

Industrial and commercial energy storage: high sensitivity of peak valley price difference, focusing on the implementation of relevant policies

The revenue model of industrial and commercial energy storage is arbitrage of peak valley price difference and increasing the proportion of photovoltaic self use. The revenue model of industrial and commercial energy storage is similar to that of overseas household energy storage, which can be divided into:

1) Save electricity charges by increasing the proportion of photovoltaic self use. If industrial and commercial enterprises build distributed photovoltaic power stations, the configuration of energy storage can store the electricity originally used for grid connection for their own use, increasing the proportion of photovoltaic power generation for their own use;

The peak valley price difference of industrial and commercial industry in each province is different, and the economic benefits of industrial and commercial energy storage are quite different. Different provinces have different electricity prices. The peak valley price difference in Beijing, Guangdong, Hubei, Jiangsu, Zhejiang and other places is large, exceeding 0.74 yuan/kWh, of which the peak valley price difference in Beijing exceeds 1 yuan/kWh. Therefore, the peak valley price difference income of industrial and commercial energy storage in the above regions is large. The peak valley price difference in Yunnan, Guangxi and other places is low, and the economy is generally poor.

We calculate that the internal rate of return of industrial and commercial energy storage is 5.3%. The core assumptions of the model are as follows:

1. The installed capacity of energy storage is 1MWh; 330 days of operation per year; Battery replacement cycle is 8 years

"Power sales through walls" is expected to promote the sharing of energy storage mode on the user side and promote the development of industrial and commercial energy storage scale. "Power sales across walls" means that distributed power generation projects are traded nearby. "Power sales across walls" allows distributed energy projects to directly sell power to surrounding users through distribution networks. This process reduces grid participation and intermediate costs. Since the end of 2021, "selling electricity through walls" has appeared in important national policy documents for many times as a high-frequency word. For the user side, the distributed power supply "wall to wall" mode can be considered as a whole near the industrial and commercial or industrial park, which is conducive to large-scale energy storage and cost reduction; For investors, large-scale user side energy storage is expected to expand the business model, thereby improving the economy; For the power grid, large-scale energy storage may become a flexible resource that can be called. We believe that the industrial and commercial energy storage is expected to develop in scale in the future with the continuous improvement and gradual implementation of the policy of "selling electricity through walls".

Frequency modulated energy storage: unstable economy, benefit the first mover

According to Greenpeace: Research on Multiple Ways to Improve the Flexibility of China's Power System, frequency modulation is divided into primary frequency modulation, secondary frequency modulation and tertiary frequency modulation. When the power grid is impacted by load shocks or new energy fluctuations, the power frequency fluctuations are larger than the safe range of the power grid, and frequency modulation is needed to help stabilize the power grid frequency. FM resources can be divided into three types: primary, secondary and tertiary control standby, corresponding to primary, secondary and tertiary FM respectively.

1) The primary reserve capacity is enabled within 5 seconds after the interference occurs, which is used to stabilize the grid frequency, and the startup time is 30 seconds. The primary frequency regulation is generally responded by the speed regulation system of the generator set;

2) The secondary control backup is to convene the backup provider within 30 seconds after the first power change, balance the control area, make the grid frequency return to the nominal value, and replace the primary backup. The startup time is 5 minutes. The secondary frequency modulation is regulated by the spontaneous generation control system (AGC); 3) The tertiary control backup is manually enabled 15 minutes after the interference, which does not completely replace the secondary control backup, and the startup time is 15 minutes. Tertiary frequency modulation is used to coordinate the economic distribution of load among power plants according to the slow changing and regular load.

Electrochemical energy storage has performance advantages in secondary frequency modulation, and the demand for frequency modulation energy storage is broad. The traditional automatic generation control (AGC) of thermal power plants has poor command tracking performance, which has problems such as low frequency modulation accuracy, reverse regulation, long response time, low regulation rate, etc. However, electrochemical energy storage has the advantages of fast regulation speed, high regulation accuracy, short response time, bidirectional regulation, etc. It can fully meet the power change demand of secondary frequency regulation within the time scale. The effect of secondary frequency regulation is significantly better than that of hydropower units, natural gas units, and coal-fired units. According to the Application of Battery Energy Storage Technology, the frequency regulation efficiency of the energy storage system with a continuous charge/discharge time of 15 minutes is about 1.4 times that of hydropower units, 2.2 times that of gas units and 24 times that of coal-fired units. And with the increase of the proportion of new energy power generation, the impact of the fluctuation of new energy on the power system increases. The lower the tolerance of grid frequency changes, the more frequent the grid frequency changes. Therefore, we believe that the demand for electrochemical energy storage and frequency modulation is large.

The benefits of FM energy storage mainly come from capacity compensation and mileage compensation. According to the Price Formation Mechanism and Cost Dredging Optimization Method of Independent New Energy Storage Power Plants, 1) the capacity compensation is based on the capacity quota compensation of energy storage frequency regulation, and the calculation method is: R capacity compensation=AGC capacity * capacity compensation price. 2) Mileage compensation is compensated in the way of market bidding according to the actual mileage of energy storage, and the calculation method is: R mileage compensation=M total service fee coefficient of FM market * MF FM mileage * K FM performance index * P FM market clearing price. M1 is generally 0-2, and 1 is selected at the initial stage; K value is a comprehensive indicator of FM performance, which can be divided into three indicators: K1 regulation rate, K2 regulation accuracy, and K3 response time. The calculation methods of K, K1, K2 and K3 vary in different provinces. One calculation method is: K1=measured speed of this unit/average regulating speed of all AGC units in the control area; K2=1 - Response delay time of power generation unit/5min; K3=1 - regulation error of power generation unit/allowable regulation error of power generation unit. The higher the K value, the better the performance and the higher the mileage compensation. According to the rules of China Southern Power Grid, the maximum K1 is 5, and the maximum K2 and K3 are 1, so the maximum K value of the comprehensive index is 3.

The combined energy storage of thermal power units can greatly increase the K value and obtain higher mileage compensation. The main weakness of thermal power frequency modulation is the regulation speed. The main advantages are mature process, high regulation capacity and low cost, and the advantages of electrochemical energy storage performance are obvious. Therefore, the combination of the two can greatly improve the performance of thermal power frequency modulation, so as to obtain higher mileage compensation. According to the performance indicators of the actual power stations in Guangdong before and after the installation of energy storage, after the installation of energy storage, the adjustment rate is increased to 4.95 (+4.09), the response speed is increased to 0.98 (+0.16), the adjustment accuracy is increased to 0.97 (+0.6), and the overall K value is increased to 2.96 (+2.23), with obvious improvement effect.

The policy determines the capacity compensation, and the market pattern determines the mileage compensation. The core of capacity compensation is the capacity compensation price, which is generally determined by policies. Capacity compensation policies vary in different provinces. Fujian's capacity compensation is 960 yuan/MW in the province, and Guangdong's bid winning capacity is 3.56 yuan/MW. Therefore, the capacity compensation income policy has a large disturbance. The core of mileage compensation is mileage clearing price and K value. The mileage clearing price is determined by the FM market demand and participating enterprises. The value of K value is determined by the relative position of the unit in the whole FM market. The performance of FM units is better than other units in the market, and the K value is larger. Therefore, mileage compensation is basically determined by the market pattern. The revenue model of FM energy storage is greatly affected by the external environment as a whole. At present, the disturbance of policies and new entrants will greatly affect the revenue rate of FM energy storage.

We estimate that the yield of FM energy storage is expected to reach 8.2%. The core assumptions of the model are as follows:

1. The installed capacity of energy storage is 150MW/300MWh; 290 days of operation per year; The operation time is 10 years.

2. FM energy storage has high performance requirements. The unit investment in energy storage is 2.3 yuan/Wh, and the proportion of self owned funds is 30%.

The internal rate of return of FM energy storage is highly sensitive to K value and mileage price, which benefits the first mover, but it is easy to enter the "Red Sea" under the interpretation of the market. Our K value is set to 1.5. In fact, at the initial stage of frequency modulation energy storage, since most of the original frequency modulation units are thermal power, the electrochemical energy storage frequency modulation has a large K value based on the comparative advantage of performance, so the income is high. The high income promotes the increase of new entrants to the market. On the one hand, the new entrants have lowered the price of FM history, on the other hand, they have improved the overall performance center, and the K value decreases accordingly. For example, the K value of a certain fire storage FM project in Guangdong has risen to 2.96, which is at the forefront of the industry. However, the relative position of the performance of Guangdong fire storage FM project will decline with the massive construction of other FM energy storage projects, that is, the K value decreases. The decline of FM mileage price and K value will greatly reduce the revenue of FM energy storage, but the projects that have been launched will not stop running. Finally, the overall market will change from high income to low income "Red Sea". Generally speaking, there are few new market entrants, the electrochemical energy storage or fire storage joint commissioning performance is relatively high, and the first mover has more compensation income and higher income.

The construction of FM market rules is still not perfect, and the implementation of relevant policies is concerned. The results of economic measurement and sensitivity analysis show that the FM market is unstable and the market rules need to be further improved. Guangdong, as the first province to develop FM market, experienced a "roller coaster" curve in the mileage compensation market throughout the year, and the average annual compensation increase from 2019 to 2020 was nearly doubled. Later, in 2021, Guangdong changed the calculation method of K value to the root of K value to weaken the performance impact and curb the FM overheating market. In 2022, the comprehensive performance index K value will be opened to the third power to further weaken the performance impact. We believe that K value has a great impact on economic accounting. Electrochemical energy storage or fire storage joint commissioning has good performance indicators, leading to higher initial project income, thus increasing new enterprises, market frequency modulation resource spillover, and weakening K value impact is mainly to prevent the disorderly expansion of the market. At present, the market rules are still under construction, focusing on the calculation method of performance indicators, market clearing rules and the introduction of policies on other benefits.

FM market is at the initial stage, and new markets are gradually opening. The traditional advantages of the energy storage and frequency modulation market are in Guangdong, Shanxi, Beijing Tianjin Tangshan, Mengxi and other places. However, in 2021, only new FM energy storage projects will be put into operation in Guangdong, and more projects will be built in new provinces. According to the statistics of energy storage and power market, in 2021, the new projects (planning, construction and operation) will cover 15 provinces and cities including Guangdong, Jiangsu, Zhejiang and Fujian, involving nearly 40 projects. The FM market is gradually opening. In the initial stage of the new market, there are not many enterprises entering the market. The K value of electrochemical energy storage and the clearing price are relatively high, so the income is high. The new market is gradually opened, and the FM market has broad prospects.

Independent energy storage: diversified income models and increased investment enthusiasm

The policy of independent energy storage continues to increase, and the business model is going out. In the overall direction, relevant policies continue to promote independent energy storage out of the business model. For example, it is proposed that new energy projects can lease independent energy storage capacity, promote independent energy storage to participate in power market transactions, and play the role of peak shaving and frequency modulation. From the trend, improving the power market system and promoting independent energy storage to participate in spot transactions in the power market are the focus of policy. In addition, provinces are constantly trying to increase the revenue channels of independent energy storage. For example, the Shanxi Energy Regulatory Office has issued the Detailed Rules for the Implementation of Shanxi Electric Power Primary Frequency Modulation Market Transactions (for trial implementation), which states that from July 1, 2022, the primary frequency modulation market of electric power will be officially opened. Independent energy storage power stations can sign contracts with wind enterprises for part of their capacity, and the rest can participate in the primary frequency modulation market independently, effectively increasing the utilization rate of independent energy storage.

The independent energy storage is connected to the power supply and the power grid, with rich revenue models. The independent energy storage is invested and operated by the investor. The construction scale is generally large, and the income model is relatively rich: 1) The independent energy storage can lease part of the capacity to the new energy side, so that the new energy projects can meet the policy requirements for allocation and storage; 2) Independent energy storage can cooperate with peak regulation and frequency modulation dispatching on the grid side to obtain compensation income; 3) The independent energy storage can cooperate with the traditional units, that is, the fire storage joint commissioning, to increase the frequency modulation performance of the traditional units and obtain the auxiliary service income; 4) Independent energy storage can participate in arbitrage in the spot electricity market, and can obtain compensation income from capacity price in some provinces.

At present, the revenue model of independent energy storage has been implemented as follows: capacity lease+spot electricity market+capacity price compensation; Or capacity leasing+peak shaving auxiliary service; Or capacity leasing+FM service. The profit model of independent energy storage projects in some provinces has been basically established. The business model of Shandong independent energy storage power station is relatively clear, and the income sources are mainly capacity lease fees, spot electricity market, capacity price compensation, etc; The profit model of Ningxia independent energy storage power station is mainly "energy storage capacity leasing+peak shaving auxiliary service"; Shanxi proposes that the independent energy storage power station can sign a contract with the wind and solar enterprises for some of its capacity, and the remaining part can provide auxiliary services for the system in the form of market bidding.

We calculate that the yield of independent energy storage is 6.7%. The core assumptions of the model are as follows:

1. The installed capacity of energy storage is 200MW/400MWh; 330 days of operation per year; The operation time is 15 years.

2. Independent energy storage has high performance requirements. The unit investment in energy storage is 2.00 yuan/Wh, and the proportion of self owned funds is 30%.

The capacity compensation price varies from province to province, including 260 yuan/kW · year in Henan, 350 yuan/kW · year in Shandong, and 470 yuan/kW · year in the estimation of the feasibility study of the Hunan project. Our neutral assumption is 330 yuan/KW · year, and the capacity lease proportion is 80%.

The service price of energy storage and peak shaving is generally 0.2-0.6 yuan/KWH, and the energy storage pilot in Ningxia can reach 0.8 yuan/kwh. We assume that the peak shaving service compensation is 0.5 yuan/kWh, and the peak shaving frequency is 300 times per year.

The internal rate of return of independent energy storage is highly sensitive to unit installed investment, capacity lease price and peak shaving service price. We calculated that the unit installed investment decreased by 0.1 yuan/Wh, and the internal rate of return increased by about 4pct; The price of peak shaving service increased by 0.05 yuan/kWh, and the IRR increased by about 4pct; The capacity lease price will increase by 30 yuan/KW * year, and the IRR will increase by about 3 pct. We believe that at present, independent energy storage has gained revenue, and for some provinces with high peak shaving service prices and capacity lease prices, the yield of independent energy storage is higher than our estimates. In addition, the position of independent energy storage in the power system is increasingly improved, and the policy is constantly exploring and improving the revenue model. The future marginal profit rate of independent energy storage is better.

The investment enthusiasm of independent energy storage has been significantly improved, and the overall large-scale development of independent energy storage has been achieved. From the perspective of installed capacity, the newly planned and under construction large energy storage projects will increase significantly in 2021. The newly added installed capacity of projects above 10MW in China is only 1.9GW, while the newly planned and under construction installed capacity will reach 23.2GW; For projects above 50MW, the total installed capacity of new projects put into operation is 0.8GW, while the total installed capacity of new projects under construction/planning is 20.3GW; For projects above 100MW, the newly added operation is 0.74GW, and the newly added projects under construction and planning are 15.8GW; In addition, the large-scale energy storage installation has reached a new level. In 2021, it is planned to build 5 projects with a total capacity of more than 500MW, totaling 5.6GW. In terms of the number of projects, the proportion of projects below 10MW will decrease. In 2021, 276 new projects will be put into operation, while the planned number is only 186. There are 304 new planned projects for projects above 10MW.

|