| Annual strategy of energy storage industry in 2023: the business model is gradua |

| Release time:2023-01-05 10:32:11| Viewed: |

Annual strategy of energy storage industry in 2023: the business model is gradually clear, and the domestic energy storage capacity is about to be released

1. Energy storage: the key link of new power system

1.1 New power systems featuring high proportion of new energy access face new challenges

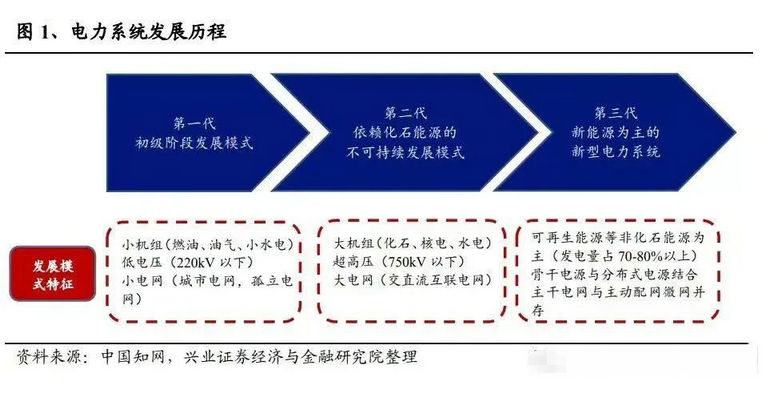

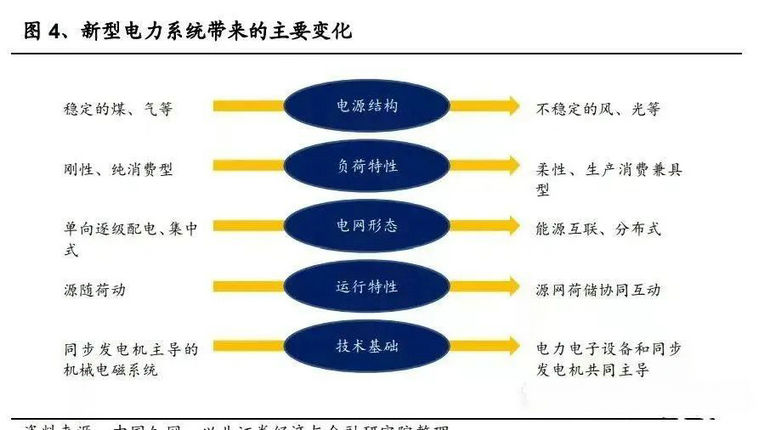

Building a new power system is the basic path to achieve "carbon neutrality". Under the background of "carbon neutrality", China's non fossil energy will account for more than 25% of the primary energy consumption structure by 2030. To achieve the goal of carbon neutrality by 2060, the future energy structure will be dominated by electricity, and the production of electricity will be switched to clean energy. Therefore, building a new power system with new energy as the main body is an important guarantee and basic path to realize the transformation of China's energy structure and achieve the goal of "carbon neutrality". The new power system takes new energy as the main body, intelligence as the means, and integration of source, grid, load and storage as the support. The new power system is a clean, low-carbon, safe, controllable, flexible, efficient, intelligent, friendly, open and interactive power system with new energy as the main supply, energy and power security as the basic premise, power demand for economic and social development as the primary goal, a strong smart grid as the hub platform, and multiple energy complementation as the support. The new power system has the characteristics of "two high", that is, high proportion of new energy and high proportion of power electronics. Replace thermal power generation with new energy, replace fossil energy with electricity, realize clean power production and electrification of terminal fields such as transportation, construction and industry, so as to realize decarbonization of the entire energy structure.

The proportion of non fossil energy power generation and terminal electrification rate will exceed 90% in 2060. The key changes of the new power system are the proportion of non fossil energy in primary energy consumption, the proportion of non fossil energy power generation in total power generation, terminal electrification rate, etc. The new power system needs to significantly increase the proportion of non fossil energy in primary energy consumption, reaching 89% by 2060; The proportion of electricity in terminal energy consumption will be greatly increased, reaching 91.82% in 2060; The proportion of non fossil energy power generation in total power generation will be significantly increased to 92.73% by 2060. High proportion of new energy access brings new challenges to the power system. Taking renewable energy as the main power generation terminal will bring about changes in the power generation characteristics of the power system, especially the imbalance between wind and solar output and load, so the problem of wind and light abandonment needs to be solved urgently.

The new power system is facing new challenges: 1) Power generation side: the proportion of wind power generation is rapidly increasing. Due to the volatility and intermittency of wind and power, with the increase of its penetration rate in the power system, new wind and power projects are difficult to access orderly, connect efficiently to the grid, regulate consumption, etc. 2) Power side: the degree of social electrification is improved, new energy users are increased, there are more peak load shocks, and load instability is increased. The challenges of new energy installation on absorptive capacity are gradually emerging. As of August 2022, the installed capacity of domestic wind power accounts for 13.97% and the installed capacity of photovoltaic accounts for 14.19%. The rapid increase of the installed capacity of new energy poses a challenge to the power grid's absorptive capacity, and the necessity of strengthening the construction of energy storage system gradually appears.

1.2 Energy storage is a key link in building a new power system

Energy storage is an indispensable key link in building a new power system. To build a new power system, it is necessary to shift from "source network load" to "source network load storage". Energy storage is a key link and an important driver in the transformation of energy structure. Accelerating the development of energy storage industry is crucial to building a clean and stable energy supply system and a healthy and safe energy consumption system.

Energy storage is essentially a solution to the problem of mismatch between energy supply and demand, which is crucial to the coupling of energy production and consumption. It has the functions of balancing real-time power, improving power system capacity coefficient, transferring energy, etc. 1) On the power supply side, the energy storage system can improve the imbalance between the new energy output and the load in time and space, reduce the waste of wind and light, and improve the new energy consumption capacity; 2) On the grid side, the energy storage system can reduce the demand for grid expansion, reduce the cost of grid construction, and improve the security and stability of the grid; 3) On the user side, the energy storage system can bring about arbitrage of peak valley price difference, reduce the cost of electricity consumption, and the distributed energy storage can also improve the user's own power control ability.

2. The top-level design is constantly improved and the pace of marketization is rapid

2.1 Solve the development pain points of new energy storage industry and realize sustainable and healthy development of energy storage

China's new energy storage industry has gradually entered the initial stage of commercialization. The development of China's new energy storage industry has gradually entered the initial stage of commercialization from the early stage of demonstration application. According to the planning of the Guiding Opinions on Accelerating the Development of New Energy Storage, China's new energy storage industry will enter the stage of large-scale development by 2025, and achieve comprehensive market-oriented development by 2030. In order to achieve the development goal of new energy storage, there are two major pain points: 1) The problem of revenue model needs to be solved urgently. On the income model: on the one hand, the income model needs to solve the problem of "inconsistency between cost subject and benefit subject". Historically, the costs related to energy storage and auxiliary services are mainly shared by the power generation side. At present, the investors and beneficiaries are unified by establishing a shared energy storage business model, incorporating capacity pricing into the scope of income and other initiatives. On the other hand, the income model also needs to solve the problem of "single source of income". With the continuous improvement of TOU price mechanism and electricity ancillary service market mechanism, and the expansion of energy storage revenue channels, the problem of single revenue source is expected to be further alleviated. 2) Cost and safety issues need to be optimized. On the one hand, technology development promotes the benefit scale of existing battery energy storage system, and continuous cost reduction will further effectively solve the cost problem. On the other hand, a variety of new technologies continue to enter the experiment, pilot demonstration and commercial operation, promoting energy storage to achieve cost reduction and efficiency increase.

2.2 Top level design continuously improves the energy storage business model

The top-level design continuously improves the energy storage business model. Since 2021, the system for the business model of the energy storage industry has been continuously optimized to improve the business environment for the development of new energy storage: In July 2021, the National Development and Reform Commission issued the Guiding Opinions on Accelerating the Development of New Energy Storage, clarified the development plan of energy storage, and proposed a scale plan of more than 30 million kilowatts by 2025; In December 2021, the National Energy Administration issued the Regulations on the Administration of Electric Power Grid Connection Operation and the Administrative Measures for Electric Power Auxiliary Services, adding new types of energy storage as independent market players, adding new varieties of auxiliary services such as inertia, climbing and leveling, establishing a sharing mechanism for user participation, which will substantially benefit the development of the energy storage industry; In March 2022, the National Energy Administration issued a notice on promoting the construction of the spot power market, specifying that the construction of a unified national power market system should be accelerated to promote the optimal allocation of power resources in a market-oriented manner.

2.3 Accelerate the marketization of new energy storage through multiple approaches

Accelerate the marketization of new energy storage through multiple approaches. In the Implementation Plan for the Development of New Energy Storage in the "Fourteenth Five Year Plan" issued by the National Development and Reform Commission and the Energy Administration, it is clear that new energy storage should be promoted to participate in power market transactions as an independent subject, new business models such as sharing energy storage should be promoted, and the capacity pricing mechanism of energy storage power stations and the peak price mechanism on the user side should be implemented to effectively promote the marketization of new energy storage. China's energy storage industry is in a critical transition period to market driven. The introduction of this plan will greatly benefit the accelerated development of China's energy storage industry in the next five years.

3. Focus on sharing independent energy storage in front of the table, and preliminary economic benefits in the back

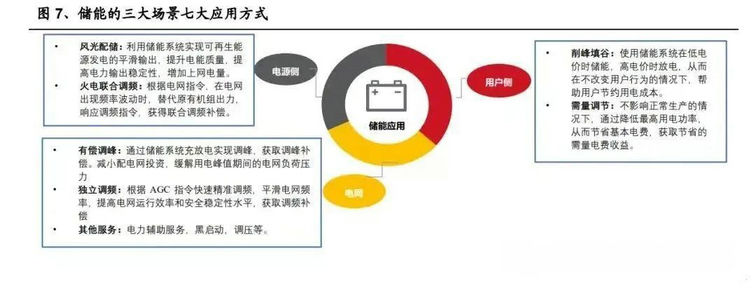

Energy storage has a wide range of application scenarios, which can be divided into three scenarios and seven application modes: power supply side, power grid side and user side.

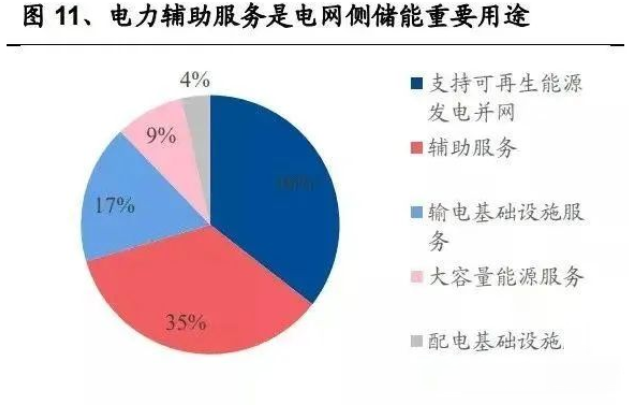

Power side: (1) Wind and solar energy distribution and storage: use the energy storage system to realize the smooth output of renewable energy power generation, improve the power quality, improve the stability of power output, and increase the online electricity; (2) Combined frequency modulation of thermal power: according to the power grid command, when the frequency fluctuation occurs in the power grid, replace the output of the original unit, respond to the frequency modulation command, and obtain the combined frequency modulation compensation.

Grid side: (3) Paid peak regulation: peak regulation is realized through charging and discharging of energy storage system to obtain peak regulation compensation. Reduce the investment in distribution network and relieve the load pressure during peak power consumption; (4) Independent frequency modulation: fast and accurate frequency modulation according to AGC instructions, smooth the grid frequency, improve the grid operation efficiency and security and stability, and obtain frequency modulation compensation; (5) Other services: auxiliary power services, black start, voltage regulation, etc.

User side: (6) Peak shaving and valley filling: use the energy storage system to store energy at low electricity prices and discharge at high electricity prices, so as to help users save electricity costs without changing user behavior; (7) Demand adjustment: under the condition of not affecting normal production, reduce the maximum power consumption to save the basic electricity cost and obtain the saved electricity demand income. The pre meter application is still the main source of domestic installed capacity. According to CNESA data, in 2021, 41% of the new energy storage capacity in China will come from the energy storage at the power supply side and 35% from the energy storage at the grid side. In total, the application before the table will account for 76% of the domestic energy storage capacity in 2021. From the perspective of power side splitting, new energy distribution and storage is still the core downstream application of power side energy storage, accounting for more than 70% of power side installed capacity in 2021.

Compulsory allocation and storage of new energy provides strong support for the development of power side installation. In the Notice on Encouraging Renewable Energy Power Generation Enterprises to Build or Purchase Peak shaving Capacity to Increase the Scale of Grid Connection issued by the National Development and Reform Commission in July 2021, it is clearly proposed that the installed scale of renewable energy beyond the guaranteed grid connection of grid enterprises should be built according to the link ratio of 15% of power. Under the background of gradually increasing pressure on new energy consumption, since the second half of last year, all regions have gradually clarified the requirements for mandatory allocation and storage of new energy.

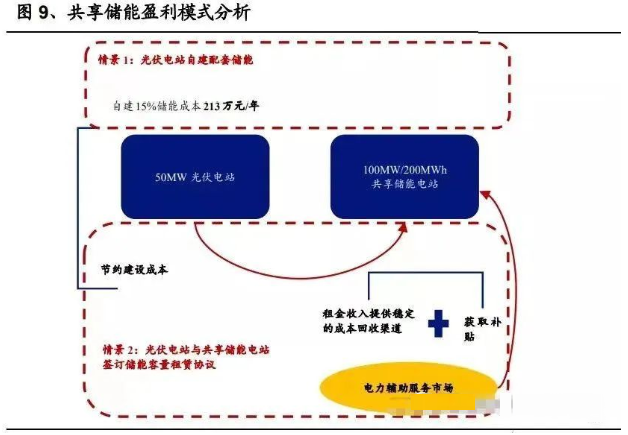

The allocation and storage of photovoltaic power station is still not economical, and the shared energy storage is better than the self built energy storage. Assuming that the annual utilization hours of the photovoltaic power station are 1300 hours, the power rationing rate is 5%, the allocation and storage ratio is 15%, and the allocation and storage time is 2 hours, the annual working days of the energy storage system are 330 days, the profitability of the energy storage configuration for the photovoltaic power station through self construction will be reduced, and the IRR will be 1.32% lower than that without allocation and storage; If the allocation and storage of the power station is completed by leasing and sharing energy storage, the IRR is 5.69% at the rent of 300 yuan/kw/year. Although it is still lower than that without allocation, the IRR is 0.28% higher than that of self built energy storage.

Shared energy storage has multiple advantages such as easy scheduling, controllable quality, and diversified income. Compared with the "1 to 1" traditional energy storage project, the "1 to N" shared energy storage will significantly shorten the investment recovery cycle and improve the project profitability. 1) Cost: reduce the construction cost of distribution and storage under the scale effect, save the daily operation and maintenance cost, and promote the scientific consumption of new energy; 2) Revenue: "One station for multiple purposes" participates in peak shaving, frequency modulation and other auxiliary power services. The rental income is superimposed with subsidy income, and the IRR is expected to reach more than 8%. In the future, with the technological progress superimposed on the scale effect, the cost of shared energy storage per kilowatt hour will be close to the pumped storage level during the "15th Five Year Plan" period, and the income prospect is considerable. At present, the total scale of shared energy storage projects has been announced to exceed 12GW/24GWh. By the end of 2021, a total of 84 shared energy storage projects have passed the filing or publicity, mainly distributed in 9 provinces such as Inner Mongolia, with the total scale of projects exceeding 12GW/24GWh. Hubei Province has the largest number of projects, 24 in total. At the same time, the scale of single shared energy storage project is getting larger and larger, and the supporting time is 2 to 4 hours. At present, there are 7 projects with a scale of 1GWh, including 6 in Hebei Province and 1 in Ningxia Province..

The multi region policy clearly proposes to develop shared energy storage. In 2021, Ningxia, Qinghai, Shandong and other seven provinces have clearly proposed the construction and development of shared energy storage in their policies, and Yiwu has also issued detailed rules to encourage the promotion of the shared energy storage business model.

The energy storage on the grid side is mainly used to support renewable energy grid connection and power auxiliary services. Auxiliary power service refers to the power generation side grid connected main bodies such as thermal power, hydropower, nuclear power, wind power, photovoltaic power generation, photothermal power generation, pumped storage, self owned power plants, new energy storage such as electrochemical, compressed air, flywheel, traditional high load industrial load, industrial and commercial interruptible load Services provided by adjustable loads (including aggregators, virtual power plants, etc.) that can respond to power dispatching instructions, such as electric vehicle charging network. The principle of "who provides, who benefits; who benefits, who undertakes" shall be followed for auxiliary power services. As for the auxiliary power service for the overall operation of the power system, the compensation cost is shared by the grid connected entities at the generation side, the market-oriented power users and other grid connected entities; For the auxiliary power services for grid connected entities or specific power users on the specific generation side, the compensation cost shall be shared by the grid connected entities or relevant power users on the relevant generation side.

It is not economical for independent energy storage to participate in peak shaving. The reform of electricity price marketization is an important direction in the future. Taking Shandong 100MW/200MWh independent energy storage power station as an example, without considering capacity leasing, it is assumed that the cycle life of the energy storage system is 6000 times, the number of annual calls is 300 times, the EPC cost is assumed to be 2 yuan/Wh based on the recent bid winning price, and the IRR is only 2.32% when the peak valley price difference is 0.6 yuan/KWh. The economy of independent energy storage participating in peak shaving alone is poor.

The realization of the economy of independent energy storage participating in peak shaving still needs to be greatly optimized. Under the requirement of 8% IRR, based on the current peak valley price difference of 0.6 yuan/KWh, the EPC cost needs to be reduced to about 1.3 yuan/Wh to be economical; If the EPC cost of 2 yuan/Wh is assumed to be unchanged, the peak valley price difference corresponding to the peak valley price difference exceeds 0.9 yuan/KWh, the independent energy storage and peak shaving will also be economical, and there is still much room for optimization.

Capacity leasing helps improve profitability. Independent energy storage can improve its own rate of return by leasing capacity to new energy power generation enterprises to obtain stable rental income. At the current rental price of 150000 yuan/MW and 20% rental ratio, the IRR of the independent energy storage power station can be increased to 4.80%.

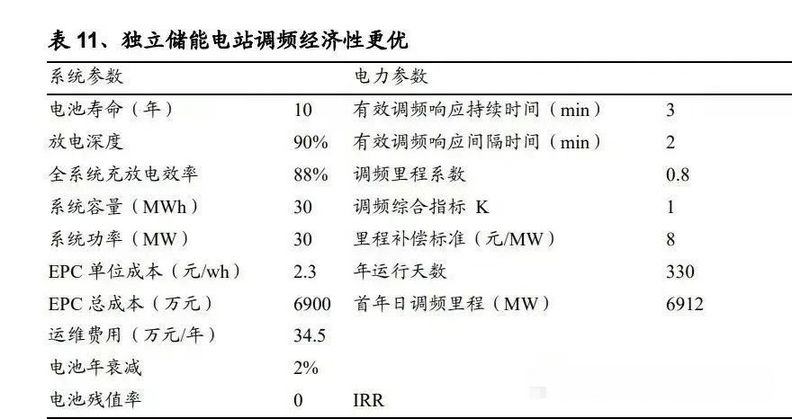

The frequency modulation of independent energy storage power station is more economical. Taking the 30MW/30MWh independent energy storage power station in Shandong Province as an example, assuming the battery life is 10 years, the effective frequency modulation response duration and interval are 3 minutes and 2 minutes respectively, the comprehensive frequency modulation index K is 1, the mileage compensation standard is 8 yuan/MW, and the annual operation days are 330 days. With reference to the bid winning price of the frequency modulation power station in the first half of the year, assuming that the EPC unit price is 2.3 yuan/Wh, the frequency modulation IRR of the independent energy storage power station can reach 16.81%, Compared with peak shaving, the economy is significantly improved.

The main profit models of user side energy storage are: 1) demand electricity charge management and dynamic capacity increase. The two-part electricity price is adopted for large industrial power consumption, which is composed of basic electricity price, kilowatt hour electricity price and power factor adjusted electricity price. The basic electricity price depends on the maximum demand or transformer capacity. The installation of energy storage system can reduce the peak power demand and save the basic electricity cost. The application of energy storage system can also stabilize the wave trough and avoid transformer capacity increase.

2) Demand response. The power grid uses the user energy storage system through dispatching to balance the demand and load of the power grid and provide compensation. Taking Guangzhou, which issued the detailed rules in the early stage, as an example, the subsidy cost is jointly determined by the effective response electricity, subsidy standard and response coefficient. At present, demand response is still in its early application in China.

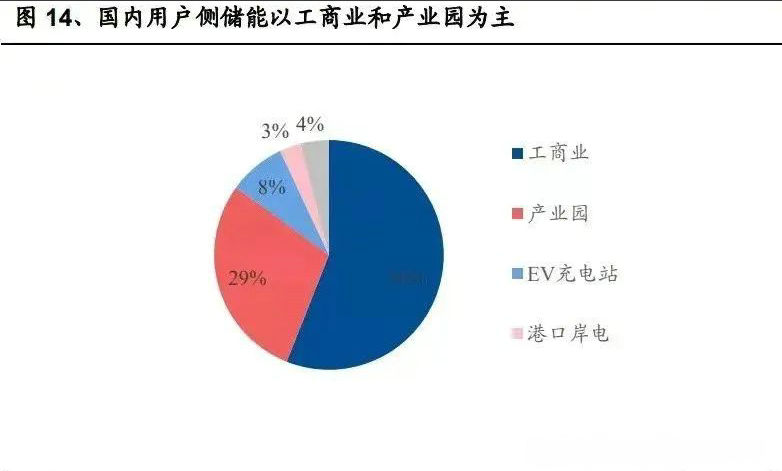

3) Electricity price arbitrage. Peak valley arbitrage is the most basic profit model of energy storage on the user side. Through charging in the valley and discharging in the peak hours, the peak valley price difference income can be obtained for profit; For distributed new energy power generation and distribution storage, it is possible to realize arbitrage of electricity price and surplus electricity on grid price and increase the income of distributed power generation system by storing surplus electricity during the peak output period of the power generation system and discharging during the low output period of the power generation system to smooth the output fluctuation. Electricity price arbitrage is the mainstream application mode of household energy storage at this stage. Domestic user side energy storage is mainly industrial, commercial and industrial parks. In 2021, the user side energy storage will account for 24% of the domestic new energy storage, which will become more and more important. According to the detailed application scenarios, the domestic industry, commerce and industrial parks will occupy the absolute main force, accounting for more than 80% in total, which is the mainstream use of user side applications.

We will improve the time-sharing electricity price mechanism and further expand the peak valley price gap. In July 2021, the National Development and Reform Commission issued the Notice on Further Improving the Time of use Tariff Mechanism, stipulating that the price difference between peak and valley prices should not be less than 4:1 in principle, and the peak price should not be less than 20% higher than the peak price. At present, 28 provinces in China have issued time-sharing electricity price policies, among which Guangdong and Chongqing can reach 0.95 yuan/kwh. Domestic user side energy storage is initially economical. Taking Guangdong 20MWh user side energy storage power station as an example, assuming that the EPC price is 2 yuan/Wh, the full life cycle IRR can reach 9.27% under the condition of two charging and two discharging per day. If the EPC unit price can be reduced to 1.5 yuan/Wh, the corresponding IRR can be increased to 16.94%, and domestic user side energy storage has preliminarily become economically viable.

Since 2022, domestic energy storage has ushered in leapfrog development. Since the beginning of 2022, the newly increased domestic energy storage bidding capacity has shown a leap forward development situation, and since the second half of the year, it has been accelerating to new heights. Affected by the rising prices of upstream raw materials, especially lithium battery materials, the average EPC bidding price has been stable at more than 1.75 yuan/Wh since this year, and the average equipment bidding price has been maintained at 1.5-1.6 yuan/Wh, which is higher than the end of last year.

In the future, as the cost continues to decline and the business model becomes increasingly mature, the energy storage market has huge development potential. It is estimated that the global new installed capacity will reach 35.5 GWh this year, which is expected to maintain high growth in the future. It is estimated that the new installed capacity will be about 300 GWh in 2025, and the CAGR will reach 97.2% in 2021-2025.

From a regional perspective, the Chinese market is an important source of energy storage installed capacity contribution. Driven mainly by the supporting energy storage at the power supply side, the domestic energy storage demand is expected to reach 10.1GWh this year, and is expected to exceed 100GWh by 2025. The domestic dry installed capacity is growing rapidly. In addition to the power supply side storage and generation capacity, the customer side installed units have great potential overseas, including household storage and industry and commerce. It is estimated that the demand for overseas energy storage is expected to reach 25.4 GWh this year and close to 200 GWh in 2025.

4. Cost safety still needs to be broken through, and energy storage optimization focuses on technical progress

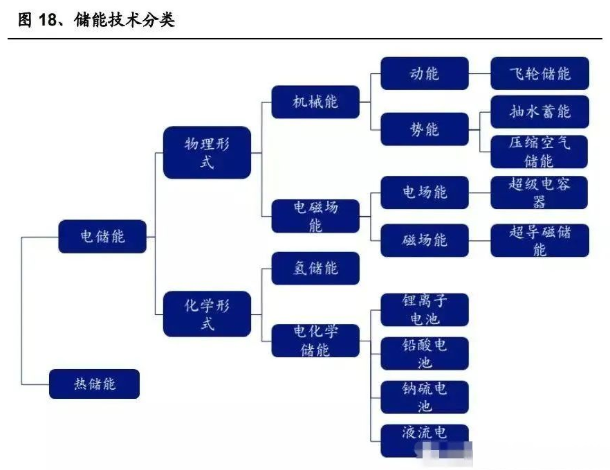

To improve the safety and economy of energy storage, the core direction is technological progress. Energy storage technology is mainly divided into electric energy storage and thermal energy storage. Electric energy storage includes physical pumped storage, compressed air storage, flywheel storage, supercapacitor, etc., as well as chemical hydrogen storage, electrochemical lithium ion battery, lead battery, liquid flow battery, etc.

The indexes for measuring different energy storage technologies mainly include rated power, response speed, etc. In different energy storage technologies, electrochemical energy storage has a fast response speed, in which the response time of lithium ion battery and lead acid battery is 1s-1 min. Pumped storage has a long response time, but it can realize high power storage. According to different requirements of energy storage duration, energy storage technology can be divided into four application types: capacity type (≥ 4h), energy type (about 1-2h), power type (≤ 30min) and standby type (≥ 15min). Among different energy storage technologies, electrochemical energy storage and hydrogen energy storage have the most flexible power and cycle coverage. The battery energy storage power can be more than 1kW-100MW, and the storage period can be up to several days; Hydrogen energy and derived gas can realize large-scale long-term energy storage under the condition of ensuring economy; The scale of hydrogen energy that can be stored is 0.1-1000MW, and the storage time is from 1 hour to several weeks.

In terms of cost, response time and power flexibility, electrochemical energy storage is the current choice of high-quality energy storage technology.

The electrochemical energy storage system mainly includes: battery system, battery management system BMS, energy storage converter PCS, energy management system EMS, etc. The cost accounts for 60%, 5%, 20% and 10% respectively. The energy storage batteries are mainly LFP batteries. From the perspective of energy storage technology category, lithium ion battery has the advantages of low pollution, high energy storage density, high charging and discharging efficiency, fast response, complete industrial chain, etc. It is the fastest developing electrochemical energy storage technology in recent years. With the gradual decline of its cost, the economy of lithium-ion batteries began to highlight. More and more new batteries used lithium-ion batteries for energy storage, and gradually replaced the existing lead batteries, which were more widely used in the energy storage market.

4.2 The cost reduction path is clear and the industrial chain needs to be improved

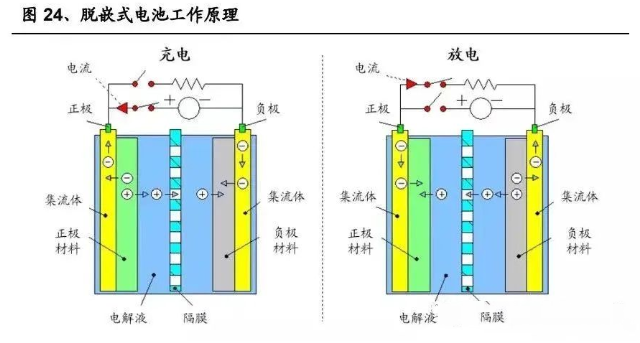

The structure of sodium battery is similar to that of lithium battery, so we can learn from the experience of lithium battery industrialization. Both sodium ion battery and lithium ion battery are rechargeable batteries, which follow the principle of de embedding. Their main structures include positive pole, negative pole, collector, electrolyte and diaphragm. When the sodium ion battery is charged, the sodium ion is separated from the positive electrode, and then reaches the negative electrode through electrolyte and diaphragm and is embedded to make the positive electrode potential higher than the negative electrode, and the external circuit electrons enter the negative electrode from the positive electrode; The discharge process is the opposite. Because sodium batteries are highly similar to lithium batteries in terms of architecture, they can be compatible in terms of battery production equipment and technology, and the production line can be switched quickly. The upper limit of theoretical energy density is lower than that of ternary lithium battery, but the energy density range overlaps with that of lithium iron phosphate battery. The energy density of sodium ion battery is 70-200Wh/kg, which does not coincide with the range of 240-350Wh/kg of NCM ternary lithium battery, and is much higher than 30-50Wh/kg of lead-acid battery; Theoretically, the high-energy sodium battery and LFP lithium battery are at the same level. The theoretical energy density of solid sodium battery is expected to even exceed 400Wh/kg, but the energy density of sodium battery that can be put into mass production at this stage has not yet exceeded the level of 160Wh/kg.

The highly deterministic long-term technical path for sodium ion to enhance energy density is "liquid → semi-solid → solid electrolyte". The technological breakthrough of positive electrode materials in the liquid battery stage also provides room for progress in energy density. From the perspective of energy density only, sodium battery is expected to first replace the low-speed electric vehicles, energy storage and other markets dominated by lead-acid and lithium iron phosphate batteries. It is difficult to move the market of consumer electronics and power batteries in the short term.

High safety, excellent high and low temperature performance. Sodium ion battery showed good capacity retention in high and low temperature tests. Since the internal resistance of sodium ion battery is slightly high, which leads to less instantaneous heat generation, there is no fire or explosion in overcharge, over discharge, short circuit, acupuncture, extrusion and other tests. The safety and stability of sodium ion battery expand the cold and transportation related markets for sodium batteries. Rapid charging has obvious advantages and long cycle life. In terms of fast charging capacity, the Stokes diameter of sodium ion is smaller than that of lithium ion, and the ionic conductivity of electrolyte with the same concentration is 20% higher, or it is allowed to use electrolyte with lower concentration to achieve the same ionic conductivity; The solvation energy of sodium ion is lower than that of lithium ion, and it has better interfacial ion diffusion ability. In terms of cycle life, the theoretical cycle of sodium battery can reach 10000 times, which is about 3000-6000 times at present, basically equivalent to lithium iron phosphate battery.

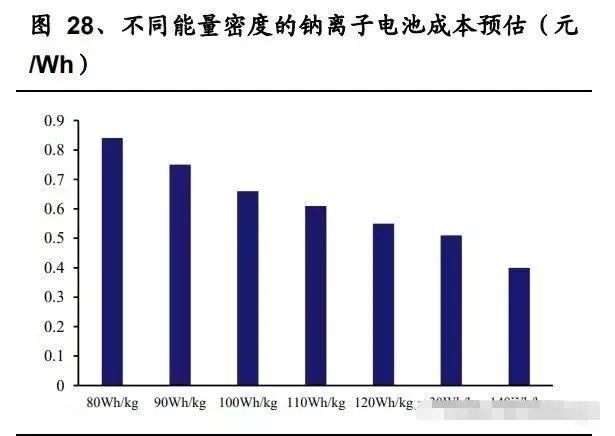

The cost node has arrived, and the energy density drives cost reduction. Compared with lithium ion battery, the material cost of sodium ion battery has 30-40% reduction space. According to the data provided by Zhongke Haina, the material cost of copper based sodium ion battery is about 0.26 yuan/Wh, which is lower than that of lithium iron phosphate battery. The material cost difference between sodium ion battery and lithium ion battery is mainly reflected in: 1) The cost of positive copper iron manganese oxide is about 1/2 of that of lithium iron phosphate; 2) The cost of coal based carbon anode material is less than 1/10 of that of lithium battery graphite; 3) Low concentration electrolyte can be used for sodium battery to reduce the cost of electrolyte; 4) The cost of aluminum foil collector in sodium battery with the same capacity is 1/3 of that of aluminum foil+copper foil collector in lithium battery.

Battery manufacturers accelerate the layout of sodium ion batteries. Against the background of the continuous high price of lithium resources, the cost advantage of sodium ion batteries is more prominent, and the production process of sodium ion batteries is similar to lithium batteries, with low switching difficulty. Mainstream battery manufacturers are accelerating the research and development layout of sodium ion batteries.

4.3 Vanadium battery: significant safety advantage, cost still to be optimized

The technology of vanadium flow battery is gradually mature. Vanadium battery, which is called all vanadium liquid flow battery, is a kind of liquid flow battery. At present, the technology has gradually matured. With its unique advantages of safety and electricity cost, it is regarded as one of the most promising electrochemical energy storage technologies in the field of medium and large energy storage.

In 1985, the all vanadium flow battery was first proposed by the University of New South Wales, and a 1kW all vanadium flow battery stack was developed in 1988. In 2002, Panzhihua Iron and Steel Co., Ltd. cooperated with Central South University in the research and development of vanadium battery. The commercialization of all vanadium flow battery was explored in China. In 2006, Dalian Institute of Chemical Physics, Chinese Academy of Sciences, successfully developed a 10kW stack. In 2009, Beijing General Energy Co., Ltd. acquired Canada's VRB power system company, holding the core patent right of all vanadium flow battery. In 2020, all vanadium flow battery energy storage demonstration projects in Dalian, Beijing and other places will be constructed successively. In May 2022, Dalian 100MW/400MWh flow battery energy storage demonstration project will be successfully connected to the grid, and will be officially put into commercial operation in August of the same year, which marks that the scale of vanadium battery technology has entered the fast lane of development. Vanadium battery has the characteristics of no solid state reaction and unchanged electrode material structure. To some extent, vanadium cell and fuel cell are similar in principle. Electrolyte is stored in two separate reaction tanks, and with the flow of electrolyte, it enters into the oxidation reaction tank and the reduction reaction tank respectively for reaction. The two reaction tanks are separated by a diaphragm. The energy efficiency of this kind of liquid flow energy storage battery depends on the voltage difference between oxidation reaction and reduction reaction, the concentration of active substances and polarization loss under different conditions. Therefore, the performance of electrolyte is the most important factor affecting the whole liquid flow battery. The positive electrolyte is composed of V (V) and V (IV) ionic solutions, and the negative electrolyte is composed of V (II) and V (III) ionic solutions. After the battery is charged, the positive material is V (V) ion solution and the negative electrode is V (II) ion solution; After discharge, the positive and negative electrodes are V (IV) and V (III) ion solutions respectively, and the battery conducts electricity through H+. The electrolyte determines the capacity, and the stack determines the power. The energy storage capacity of all vanadium flow battery depends on the volume of electrolyte and the concentration of vanadium ions. The higher the concentration and volume of electrolyte, the more vanadium ions can participate in the reaction and the more electric energy can be stored. The magnification is determined by the electrode area of the stack. The larger the electrode area of the stack, the larger the effective contact area between vanadium ion and electrode, the more electrons can pass through, and the greater the current, which is the magnification.

All vanadium flow battery has multi-dimensional advantages: high safety: vanadium ions of all vanadium flow battery exist in sulfuric acid aqueous solution, while the electrolyte of lithium battery is flammable organic solvent, so vanadium battery is less likely to overheat and explode. Although long-time operation may lead to breakage of the ion conduction membrane and mutual mixing of positive and negative active substances, it will not cause short circuit and lead to thermal runaway. During the system operation, the electrolyte circulates between the stack and the electrolyte storage tank through the pump, and the heat generated by the stack can be effectively discharged through the electrolyte circulation. The uniform distribution of liquid in all vanadium redox flow battery makes the single cells have good consistency, eliminating the system security problems caused by poor battery consistency. Easy to expand: power and capacity modules are independent of each other. The power of all vanadium flow battery is determined by the size and number of electrodes in the stack, and the capacity is determined by the concentration and volume of electrolyte. Therefore, the capacity expansion of power can be achieved by increasing the number of electrodes in the stack and the area of the stack, and the capacity improvement can be achieved by increasing the volume of electrolyte. Power and capacity are independent of each other, making the design more flexible.

Long service life: during charging and discharging of vanadium redox flow battery. Vanadium ion only changes its valence state, does not react with electrodes or other materials in solid state, and 100% deep discharge has no effect on battery life. In the static state, the positive and negative electrolyte are stored in the liquid storage tank respectively, without self discharge. The charging and discharging cycle life of vanadium liquid battery can reach more than 13000 times, and the calendar life is more than 15 years. The 25 kW all vanadium liquid flow battery module manufactured by Sumitomo Electric Co., Ltd. of Japan has been operated in the laboratory, with more than 16000 charging and discharging cycles. The electrolyte is easy to recycle and has good environmental and economic benefits: the electrolyte of all vanadium flow battery only changes in its valence state, without other side reactions. It remains active after long-term use and can be recycled and reused. The recovery of electrolyte can bring economic effect and greatly reduce the cost of electrolyte. Low cost: The cost of long-term energy storage in the whole life cycle is better than that of lithium battery.

Disadvantages of all vanadium flow battery: high initial installation cost. Due to the fact that it has not been commercialized on a large scale and is subject to equipment, capacity and high initial investment, the current cost of liquid flow battery is still on the high side. The high installation cost means that the initial investment of all vanadium liquid flow battery is large, which limits its industrialization development to a certain extent. In addition, under normal use, professional personnel should carry out maintenance every two months. High frequency maintenance makes it difficult to apply it widely on the user side. Vanadium battery still faces huge price pressure. With the promotion of policies, the cost of vanadium batteries is expected to further decline after the formation of large-scale and clustered industries. Low energy density and low efficiency. At present, the energy density of all vanadium flow battery is only 20~50Wh/kg, which is less than 1/3 of lithium iron phosphate battery. Vanadium batteries need pumps to maintain electrolyte flow in the stack, which consumes a lot of energy. The highest energy conversion efficiency is 85%, which is lower than 90% of lithium batteries. The operating temperature range is narrow. The ideal working environment of all vanadium flow battery is 5~45 ℃, beyond which heating or cooling by thermal management system is required. Once the temperature is higher than this, sediment will be precipitated in the positive electrode solution to block the flow passage, making it scrapped. At the same time, the temperature should not be lower than the freezing point of the electrolyte. If the temperature is too low, the electrolyte will solidify, while if the temperature is too high, the V5+in the solution will form V2O5, which will block the electrolyte channel and cause the battery to be scrapped. |