| The "danger" and "opportunity" of wind power industry |

| Release time:2023-02-17 09:10:04| Viewed: |

In response to climate change and changes in energy patterns, more than 130 countries and regions such as China, the European Union, the United States and Japan have put forward the goal of carbon neutrality. The use of clean energy such as wind energy, nuclear energy and solar energy has seen a leap in development. The gradual maturity of the carbon market and the rising carbon price have become the main driving force for all sectors of the world to increase investment in clean technology. At the same time, while many European countries suffered high temperatures this summer and tried to store natural gas for this winter, Russia continued to restrict the supply of natural gas, which will lead to the intensification of the "gas shortage" in Europe. Some European countries hope to take this opportunity to strengthen cooperation in the field of new energy so as to gradually get rid of the dependence on Russian fossil fuels and make contributions to the EU's carbon neutrality standards.

On August 30, the heads of state or government of the eight European countries and EU leaders held the Baltic Sea Energy Summit in Malinburg, the residence of the Danish Prime Minister, and signed the "Malinburg Declaration", agreeing to strengthen energy security and offshore wind power cooperation, and planning to increase the installed capacity of offshore wind power in the Baltic Sea region under their control from 2.8 GW to 19.6 GW (1 GW equals 1 million KW) by 2030.

In the first half of this year, the "Fourteenth Five-Year Plan" for Modern Energy System (hereinafter referred to as the "Plan") issued by China has aroused strong attention from the market. Guangdong, Fujian, Zhejiang and other coastal provinces have successively issued plans. By 2025, the installed capacity of offshore wind is expected to increase by 60GW, which is about 6.7 times the cumulative installed capacity by the end of 2020. The current operating level (24GW) has increased by about 150%. At present, China has become the country with the largest scale of offshore wind power operation in the world. The new market space in foreign countries is also quite broad. The acceleration of the installation planning in Europe and Vietnam will, to a certain extent, drive the domestic wind power industry to sea.

This paper analyzes the endogenous logic and bottlenecks of the development of wind power industry to see the internal trend of wind power development, with a view to enabling readers to fully understand the future development trend of wind power industry.

"Opportunity" of wind power industry

Figure 1 Average wind speed distribution of global land and sea wind energy distribution

In terms of global wind energy resources, the current estimated global wind energy is about 2740TW, and the regions with annual average wind speed greater than 6.9m/s (80m high) account for 13% of the global wind energy. The high altitude wind energy in these regions is about 72TW, and the capture of 20% is about 7 times of the current global power demand (2.0TW).

In Figure 1, we can see that most of the world's wind energy resources are concentrated in the contraction zone of the coastal and open continents, such as the mid-high latitude ocean surface of the southern hemisphere, the North Atlantic, the North Pacific and the mid-high latitude part of the Arctic Ocean. The continental wind energy is concentrated in the western United States, the coastal waters of Northwestern Europe, the top of the Ural Mountains and the Black Sea region, with strong regional resources.

China has the largest installed capacity of wind power in the world, but the land wind energy resources are not the richest, and the land area with high wind speed (wind force of 3-7) only accounts for 11% of the land area. In regions where developing countries are concentrated, such as the Middle East, Africa, and Latin America, there is little installed capacity and rich resources, and there is still large space for wind power development.

2、 Analysis of the industrial chain of wind farm industry

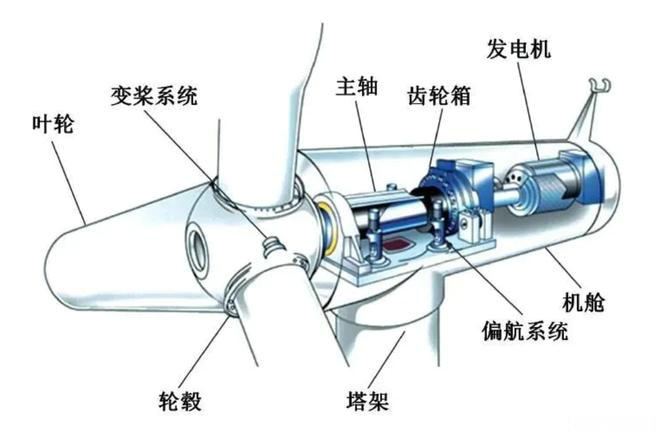

(1) Wind turbine structure

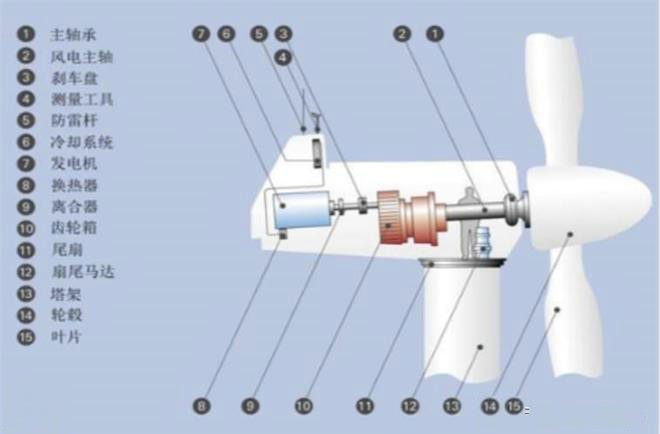

The wind turbine is composed of a base, a tower, a fan and a blade. The tower drum is not only used to raise the height of the fan, but also as a channel for transmission lines; There are various generator sets and other control equipment inside the fan; The blade is one of the key components of the wind turbine. Its design, material and technology determine the performance and power of the wind turbine generator.

Figure 2 Main structure of wind turbine (2) Wind power industry structure

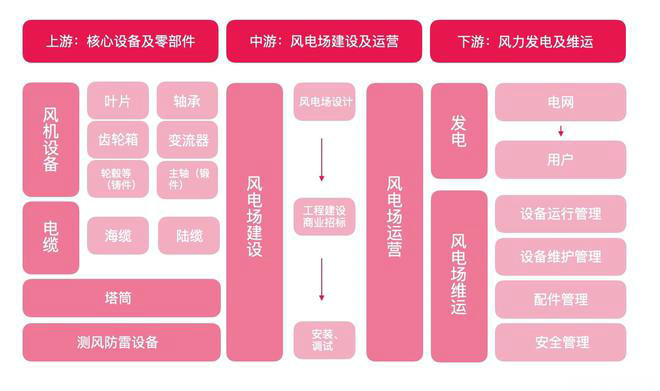

The upstream of the wind farm industry includes the core equipment of the wind farm and its components, namely, wind turbine equipment, cables and tower drums. The components mainly include blades, gear boxes, generators, bearings, castings, converters, reducers, etc. The external links also include tower drums, flanges, and submarine cables.

The midstream includes the construction and operation of wind farms;

Downstream mainly involves power generation and wind farm maintenance and operation market.

Among them, the participants mainly include the government, developers, core equipment and parts manufacturers. First of all, the operator needs to obtain the project approval document from the provincial investment authority before starting the construction of the wind farm. Due to the relatively high investment in a single wind farm, the operators are mainly large state-owned enterprises. According to the statistics of China Wind Energy Professional Committee, by the end of 2021, the cumulative installed capacity of major state-owned enterprises and groups accounted for 63% of the total national total.

Tower tower/wind turbine foundation/submarine cable: wind turbine foundation and submarine cable products are mainly purchased directly by the owner or EPC contractor, with strong engineering accessory properties, and have certain requirements for the supplier's relevant past business performance, localized manufacturing capability, etc. The downstream customer types of the tower are relatively diversified, including owners, EPC contractors and complete machine enterprises. The onshore wind power tower products themselves have strong transport radius restrictions.

Bulk commodities: From the perspective of cost, the proportion of raw materials in the cost composition of the main links of the wind power industry is generally more than 50%. The specific application of raw materials is mainly steel, copper, rare earth and other bulk commodities. The downstream application fields are wide. The fluctuation of wind power demand has no material impact on the price of related raw materials.

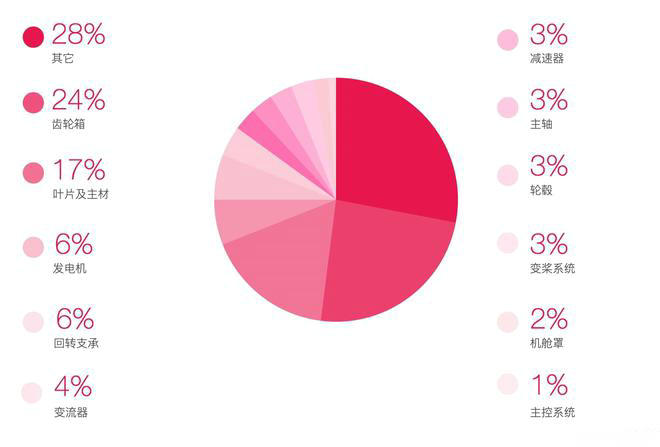

Figure 3 Industrial chain structure of wind farm industry According to the data in Sany Heavy Energy's prospectus, in the technical route of double-fed drive, gearbox, blade, generator and bearing account for a relatively high proportion of the fan cost, which are 24%, 17%, 6% and 6% respectively.

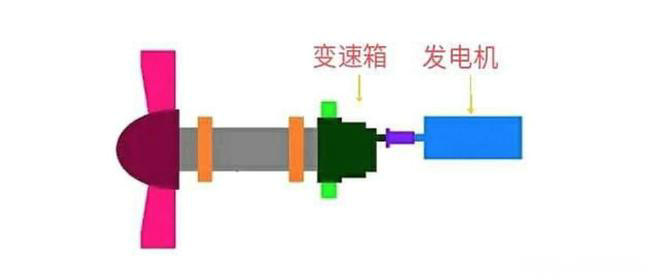

Figure 4 Schematic diagram of doubly-fed drive

Figure 5 Proportion of upstream parts cost of fan

3、 Global wind power development

In 2021, the global wind power installed capacity will increase by 93.6GW, the second highest year in history, of which 72.5GW will be installed on land and 21.1GW will be installed on sea. The cumulative installed capacity of wind power in the world reached 837GW, an increase of 12% over the previous year.

Although the new installed capacity slowed down, the new installed capacity of offshore wind power reached a record high of more than 21GW, more than three times that of the previous year.

Figure 6 Trend of new installed capacity of wind power in the world from 2001 to 2021 (GW)

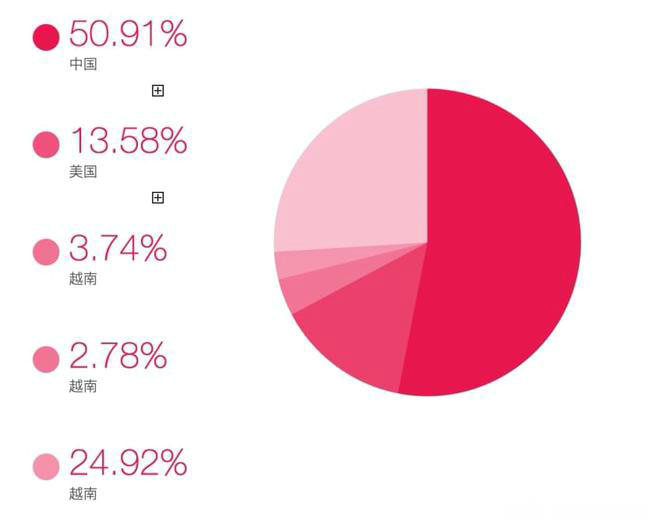

The global offshore wind power achieved 21.1 GW of new grid connection in 2021 (more than three times of 2020), creating the best record in history. China stands out, with its offshore wind power increment accounting for 80% of the global total, which also makes China surpass the UK as the country with the largest cumulative offshore wind power installed in the world.

Figure 7 Proportion of new installed capacity of global wind power in 2021 In 2021, the global wind power bidding volume was 88 GW, up 153% year on year. Although covid-19 has slowed the delivery of a large number of projects, it is still in a trend of rapid growth in terms of the global wind power bidding volume.

At present, the issue of energy security is receiving widespread attention. The conflict between Russia and Ukraine, the COVID-19 and climate change will jointly bring the energy industry to a "critical inflection point". The "Malinburg Conference" is mainly aimed at the imbalance between energy supply and demand in Europe after the Russian-Uzbekistan conflict. In order to reduce the dependence on Russian energy and solve the problem of energy security, European countries are determined to increase wind energy production in the Baltic Sea. Germany and Denmark are the only coastal countries with large wind farms in the Baltic Sea at present, and the two countries are determined to further increase production capacity. However, domestic manufacturing enterprises have begun to show their advantages of high cost performance, such as wind power components, generators, spindles, castings and other overseas orders are expected to grow rapidly in the future.

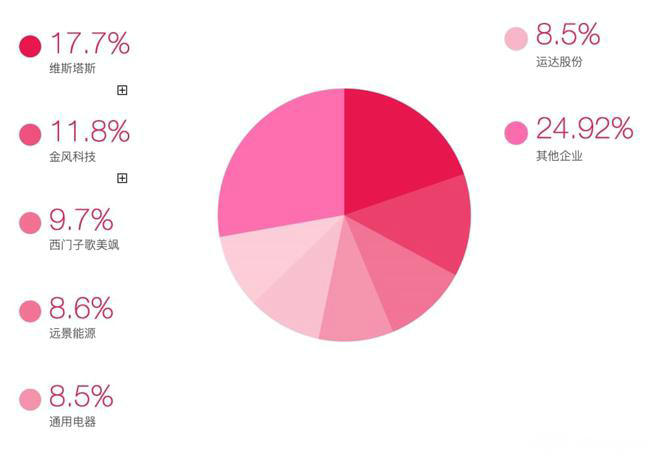

Figure 8 Generation of new wind turbines in Europe in 2021 From the perspective of global market competition, Vestas, Goldwind Technology and Siemens Gamesa ranked among the top three in the world according to the 2021 ranking of global wind power manufacturers published by Bloomberg New Energy Finance (BNEF), with a total installed capacity accounting for 36% of the global market share. Vision Energy ranks the fourth in the world, with its export volume increasing significantly, followed by General Electric (GE), which ranks the fifth.

Among the top ten complete machine manufacturers in the world, Chinese wind power enterprises occupy six seats, and the cumulative installed capacity accounts for about 44.8% of the global annual new capacity. According to BNEF data, in the ranking of global offshore wind turbine manufacturers in 2021, Shanghai Electric, Mingyang Intelligent, Goldwind Technology and China National Offshore Electric Co., Ltd. occupied the top four positions of global offshore wind turbine manufacturers, among which Shanghai Electric ranked first.

From the perspective of market share, since 2010, the share of international wind turbine manufacturers in the Chinese market has been declining. According to BNEF data, the ranking of Siemens Gomesa fell to the sixth in 2021, replaced by the rise of Chinese machine manufacturers.

Figure 9 Ranking of global wind turbine manufacturers in 2021

3、 Current situation of wind power development in China

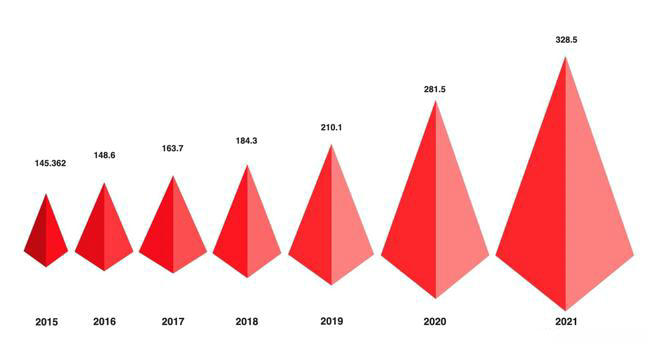

According to the data of the National Energy Administration, the cumulative installed capacity of wind power in China will reach 328.5GW in 2021, with a year-on-year growth of 16.7%, which is faster than that of the world. The cumulative installed capacity of wind power accounts for 39.2% of the world.

Figure 10 Trend of China's wind power cumulative installed capacity in 2015-2021

In 2021, China's offshore wind power installation reached a record high. In 2021, 2603 offshore units will be newly hoisted and the newly installed capacity will reach 14.482 million kilowatts, an increase of 276.7% year on year, mainly distributed in Jiangsu, Guangdong, Zhejiang, Fujian, Liaoning, Shandong and Shanghai. Among them, the newly installed capacity of offshore wind power in Jiangsu reached 4.99 million kilowatts, accounting for 34.4% of the newly installed capacity of offshore wind power in China; Next are 33.7% in Guangdong, 10.2% in Zhejiang, 9.0% in Fujian, 4.3% in Liaoning, 4.2% in Shandong and 4.1% in Shanghai.

Figure 11 Statistics of new installed capacity of wind power generation in China from 2016 to 2021

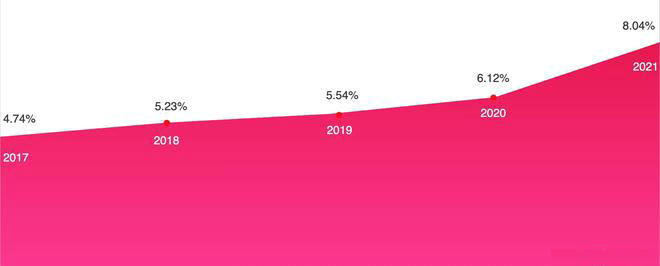

The proportion of wind power generation in the total social power generation has increased year by year. According to the statistics of the China Electricity Union, in 2021, the country's dazzled energy will be 8.38 trillion kilowatt-hours, an increase of 9.84% year on year, the renewable energy power generation will be 2.32 trillion kilowatt-hours, accounting for 27.73%, and the wind power generation will be 655.6 billion kilowatt-hours, accounting for 7.83%, and its proportion in the country's total power generation will increase year by year.

Figure 12 Trend of the proportion of China's wind power generation to total power generation in 2017-2021

In terms of technology, wind power technology is divided into large wind power technology and small and medium-sized wind power technology. Although both belong to wind power technology and work in the same principle, they belong to completely different industries, as shown in:

1. Different policy orientations

There is still a certain gap between China and the world in large-scale wind power technology. At present, domestic offshore wind turbines are mainly 6MW, while foreign countries mainly promote 13-15MW, and even develop 30MW models. Large wind turbines have strict environmental requirements. Domestic core technologies still depend on foreign countries. There are few large wind power system technologies and core technologies with independent intellectual property rights. A series of problems are still restricting the development of large wind power technologies.

However, the domestic small and medium-sized wind power technology has been in the leading position in the world. With the complete realization of independent localization of the technology, the domestic small and medium-sized wind power technology can not only be applied independently, but also be used for distributed independent power supply in combination with optoelectronics. However, due to different policy priorities, the early state has always positioned small and medium-sized wind power generation in Inner Mongolia, Xinjiang and other places, which is not enough to meet the domestic market for power generation and grid connection. However, at present, the technical progress of wind turbine large-scale is more than expected, the trend of large-scale is significantly accelerated, and the cost of industrial chain has achieved a rapid decline.

From the bidding situation this year, the unit capacity of onshore units is basically more than 3MW, and large capacity units of 4.65MW-182 and 5.0MW-191 levels also appear in the low wind speed area, and 5.0MW and 5.2MW models appear in the bidding of projects in the medium and high wind speed area. The trend of large-scale is significantly accelerated, which is a favorable condition for Longtou Company and can win more market share.

4. Market pattern of China's wind power industry

(1) Market overview

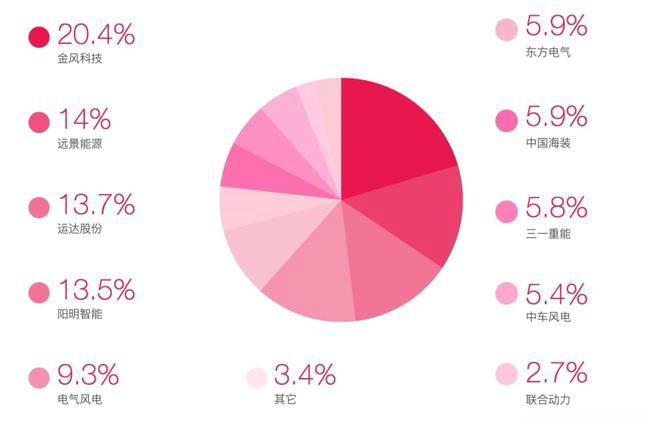

At present, the leading enterprises in the fan equipment sector include Goldwind Technology, Dongfang Wind Power, etc;

Figure 13 Leading enterprises in China's wind power industry map

Figure 14 Market share of major wind turbine manufacturers in China in 2021

In 2021, a total of 7 complete machine manufacturing enterprises have newly installed offshore wind power, of which 876 electric wind power will be newly installed, with a capacity of 4.24 million kilowatts, accounting for 29%, ranking first, followed by Mingyang Intelligent, Goldwind Technology, China National Offshore, Dongfang Electric, Vision Energy and Harbin Electric Wind Energy.

By the end of 2021, there were 13 offshore wind turbine manufacturing enterprises, among which, the total installed capacity of offshore wind turbines was more than 1 million kilowatts, including Electric Wind Power, Mingyang Intelligent, Goldwind Technology, Vision Energy, China National Offshore and Dongfang Electric. The total installed capacity of offshore wind turbine units of these six enterprises was 24.707 million kilowatts, accounting for 97.5% of the total installed capacity of offshore wind turbines.

(2) Upstream and downstream competition

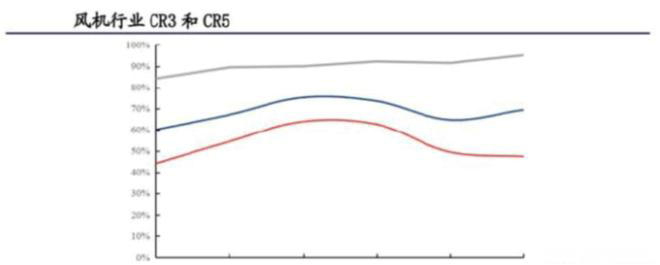

Bearing: It is one of the links with the highest odd-number barriers in the wind power industry chain. The first tier enterprises in China include Xinqianlian, Luoxi, Waxi, etc. The pattern is relatively stable and the concentration of the global market is high. With the development of large-scale wind power, the technical requirements for bearings are becoming higher and higher, and large megawatt capacity is scarce.

Figure 15 CR3 and CR5 of fan industry

(3) Operation of individual leading enterprises

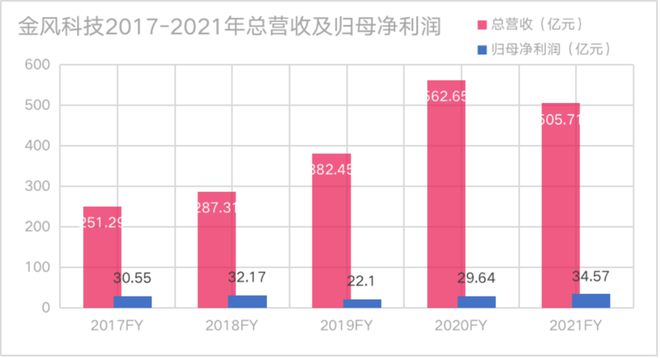

Goldwind Technology, formerly known as Xinjiang Xinfengke Industry and Trade Co., Ltd., was listed on the Shenzhen Stock Exchange in 2007. As a leading domestic wind power enterprise, Goldwind Technology deeply focuses on the three fields of wind power, energy internet and environmental protection, and promotes the utilization efficiency of renewable energy to a new level with strong scientific research innovation and best business practices.

Figure 16 Total revenue and net profit attributable to parent company of Goldwind Technology in 2017-2021

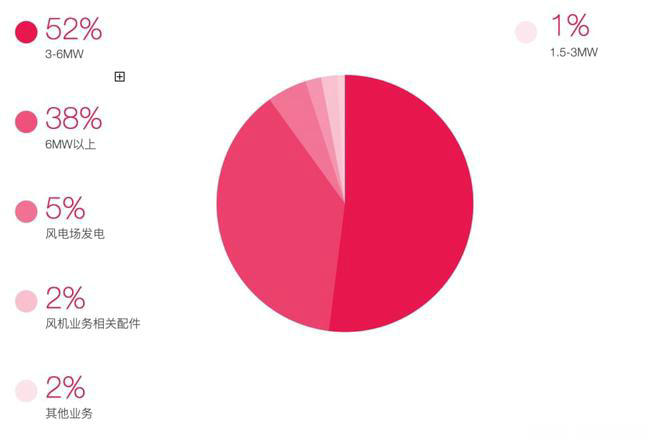

In 2021, the main revenue of Goldwind Technology is the sales of fans and parts, with the operating revenue of 39.932 billion yuan, a year-on-year decrease of 14.42%, accounting for 78.96% of the operating revenue. The second is the development of wind power plants, with an operating income of 5.327 billion yuan, up 32.56% year on year, accounting for 10.53% of the operating income.

The company's production and sales volume was 11625.95MW and 11823.22MW, down 18.25% and 14.66% respectively year on year; The main reason is that the sales volume of onshore wind power products has declined. With the end of the rush to install onshore wind power, the growth rate of onshore wind power sales of Goldwind Technology in 2021 has declined significantly. The revenue of GW2S series, which has a revenue weight of about 60% in 2020, will plummet by 61.25% by 2021. However, in 2021, the sales of offshore wind turbines were hot, and the GW6S/8S series, with a revenue weight of only about 5% in 2020, saw a significant increase of 312.18% in revenue in 2021, and the revenue weight increased to 24.01%. In addition, the revenue of GW3S/4S series of large-capacity units has achieved a rapid growth of 121.89%, and the revenue weight has increased significantly from 10.47% in 2020 to 25.85% in 2021.

After offsetting the changes in the income scale of various series of products, the annual income level of Goldwind Technology has declined, and the income growth rate is lower than that of Mingyang Intelligent, which has a higher weight of offshore wind turbine income. However, because the gross profit level of offshore wind turbines is significantly higher than that of onshore wind turbines, with the significant increase in the income right of offshore wind turbines in 2021, the gross profit rate of Goldwind Technology has increased from 17.73% in 2020 to 22.55% in 2021, and the gross profit rate has increased by 4.82 percentage points, The scale of net profit achieved a positive year-on-year growth.

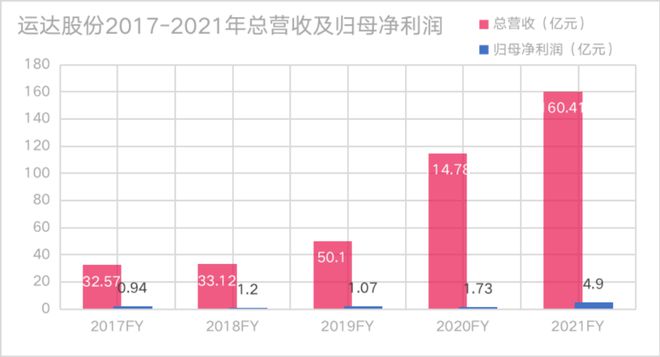

Yunda Shares

At present, the enterprise is actively developing to layout the front and back ends of the industrial chain, investment and operation business of new energy power stations and post-market smart service business. It has five production bases (under construction) in Yuhang, Hangzhou, Zhangbei, Hebei, Wuzhong, Ningxia, Harbin, Heilongjiang and Ulanqab, Inner Mongolia.

Figure 17 Total revenue and net profit attributable to parent company of Yunda Shares in 2017-2021

Mingyang Intelligence

In 2020, the company further launched the 5.2MW series of land models with 166m impeller diameter, becoming the largest unit with the largest unit capacity on land in Asia. The ultra-low wind speed technology of the company makes the 5m/s ultra-low wind speed resources also have development value by increasing the sweep area and tower height.

Mingyang Intelligent has built 13 production bases in China close to customers, including 6 complete machine production bases, 6 blade production bases and 1 power electronics production base; At the same time, six regional operation and maintenance service centers and more than 300 spare parts warehouses have been set up, and a rapid response service platform of production base+operation and maintenance service center+project has been established to ensure that personnel, spare parts and other resources can achieve low-cost transportation and rapid response in production delivery and post-market operation and maintenance services.

Figure 18 Total revenue and net profit attributable to parent company of Mingyang Intelligent in 2017-2021

Figure 19 Proportion of revenue structure of Yangming intelligent segmentation products in 2021

The "crisis" of wind power industry

1、 Subsidy recession has weak intrinsic innovation

In the past ten years of wind power, the government has implemented the wind power price and cost sharing system, from the government guidance price to the model of taking the benchmark electricity price as the main part and the renewable energy electricity price as the supplementary fund. In June 2021, the National Development and Reform Commission issued the Notice on Issues Related to the 2021 New Energy On-grid Tariff Policy, stipulating that from 2021, centralized photovoltaic power stations, industrial and commercial distributed photovoltaic and newly approved onshore wind power projects will not be subsidized by the central government and will be put on the grid at a fair price. Since 2022, offshore wind power and household distributed photovoltaic will no longer enjoy state subsidies. The new guidance price of wind power has restored the commodity attributes of onshore wind power products, and it is clear that the market is the only incentive source.

This means that the expensive offshore wind power must compete with the local coal price. In recent years, the EPC cost of domestic offshore wind power projects has declined to about 12000 yuan per kilowatt. According to industry estimates, to achieve the cost of 0.2 yuan per kilowatt of electricity, the EPC cost of offshore wind power projects should be less than 10000 yuan per kilowatt, and the annual power generation should reach more than 6000 hours.

For enterprises, the main way to achieve this is to scale up the wind turbine and increase its power. Therefore, in order to increase production capacity, enterprises have significantly increased the installed capacity. Last year, the new installed capacity was as high as 71.67 million kilowatts, a year-on-year increase of 178%. This proves to a certain extent that China's wind power enterprises have not yet formed a technology-oriented advantage, and still rely on the regulation module to compete.

Since power itself is an industry with long investment return time and high investment cost, China's patent applications are basically concentrated in the State Grid, mainly based on policy support rather than market support, and the endogenous innovation ability of enterprises is weak.

2. The cost of offshore wind power remains high

Figure 22 Main structure of wind turbine

At present, the cluster development of offshore wind power also needs to be strengthened. In order to promote the subsequent development of offshore wind power, in addition to the intensive and large-scale development mode, the construction of offshore wind power base is also of great significance. The large base can reduce the development cost of offshore wind power, and the expansion of the scale is conducive to reducing the procurement cost of equipment, as well as the costs of construction, operation and maintenance and various early stages. It is an important way to reduce costs and increase efficiency.

Prospect and prospect

1. Development direction of wind power industry

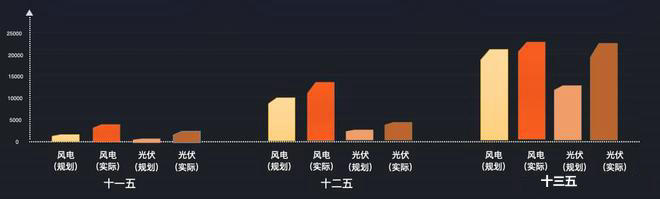

In general, during the 14th Five-Year Plan period, the total planned offshore wind power of each province exceeded 40GW, and the planned installed capacity of coastal bases exceeded 100GW. According to China's "Fourteenth Five-Year Plan" for Power Development, offshore wind power will be developed in Guangdong, Jiangsu, Fujian and other coastal areas. The document plans to build a large coastal base with the planned installed capacity of 71 million and 132 million kilowatts in 2035 and 2050 respectively. And the actual installed capacity is usually higher than the planned installed capacity. According to the past, the actual installed capacity during the 11th Five-Year Plan, 12th Five-Year Plan and 13th Five-Year Plan is much higher than the planned installed capacity.

Therefore, we expect that the installed capacity will still be greater than the planned value during the 14th Five-Year Plan period, and China's offshore wind power construction has a broad prospect. Zhongtian believes that in the eastern region, with relatively limited land resources, offshore wind power will become an important link in the development of new energy in coastal provinces in the future.

Figure 21 Actual installed capacity compared with planned installed capacity

2. Industrial technology development direction The following five development trends of offshore wind power have emerged:

1. Wind turbine parity online: offshore wind power will gradually be parity, and the cost will gradually reduce to achieve parity online.

|