| These three points determine the success or failure of the energy storage system |

| Release time:2023-02-17 10:50:40| Viewed: |

Under the background of "double carbon", the energy storage industry has stepped into the market, and the global energy storage market demand has exploded rapidly. As the midstream link of the energy storage industry chain, system integrators have become the most concerned "focus" of the energy storage industry by connecting equipment suppliers and owners of energy storage systems. The author believes that their success lies in the following three points:

1、 Technology

Energy storage integration is a system engineering, which requires unified coordination of all key equipment links. The comprehensive management of each link is the best to achieve the effect of "1+1>2". The energy storage integration enterprise purchases the core equipment externally, and then carries out the system integration. However, the coordination and consistent work of each link requires the integration ability of the integrator. The peripheral equipment can be purchased externally in the whole market, but the product performance and effect of each integration enterprise are quite different.

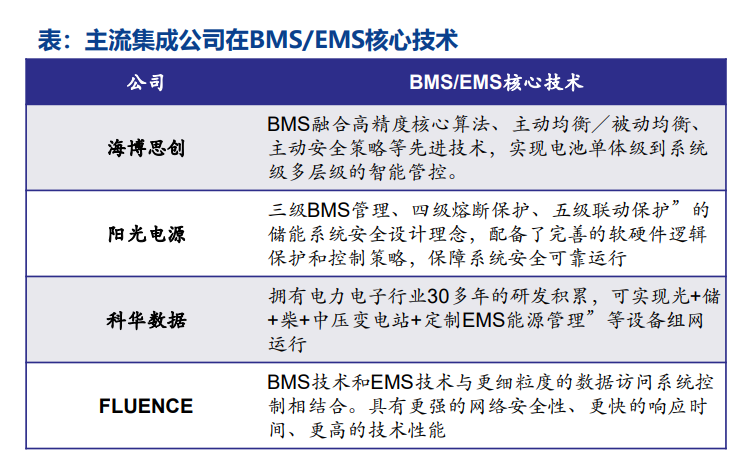

The accumulation of experience in building energy storage system is an important factor, and the management system is often built independently. Downstream application scenarios involve multiple fields, such as joint frequency regulation of thermal power plants, energy storage of new energy, peak-shaving on the grid side, valley filling arbitrage on the user side, and micro-grid in areas without electricity. The integration of energy storage requires high power grid understanding and corresponding EMS/BMS capabilities. Mainstream energy storage manufacturers may use outsourcing to support batteries and PCSs, but BMS and EMS systems involving monitoring and management are basically independently designed by integration manufacturers.

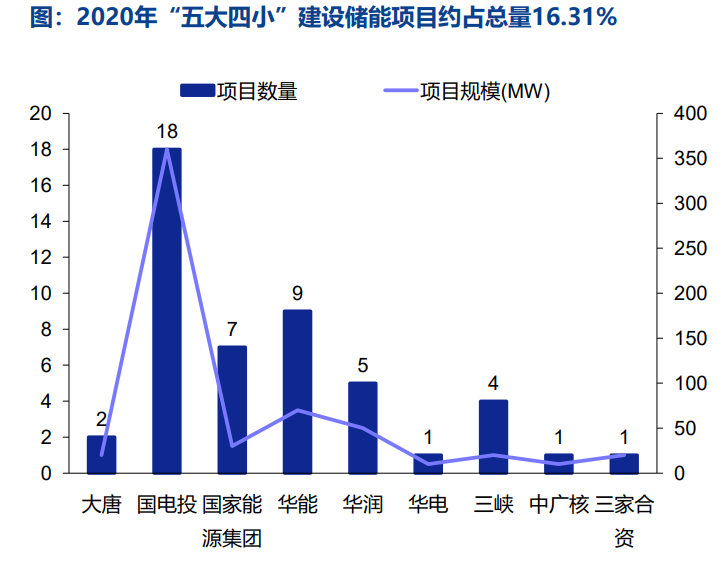

The energy storage system integration competition is fierce, and the backward technology will be eliminated. Take thermal power frequency modulation as an example, the market participants survive the fittest quickly. From the perspective of market competition, the fire storage combined FM market was relatively small before 2017. Most of the projects belonged to Ruineng Century and Kelu Electronics, with a high market share. After 2017, a large number of manufacturers poured into this field, including energy storage enterprises (Desheng Xinneng, etc.), large power grid enterprises (China Southern Power Grid, etc.), and large central enterprises (China Resources, etc.). Many new entrants drove the industry to "roll in", and competition intensified. In terms of performance, cost Enterprises with security advantages will stand out.

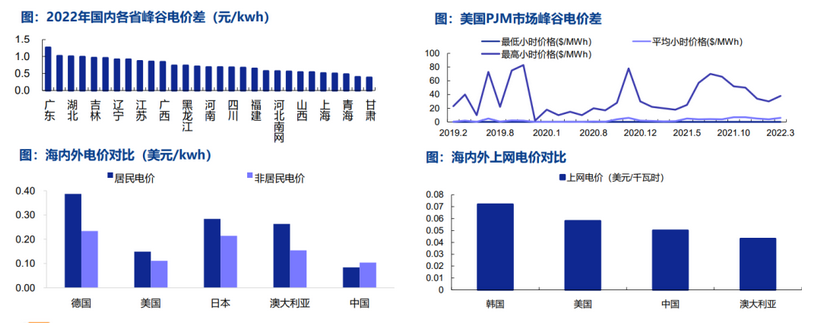

The more mature the energy storage market, the higher the requirements for technology and product stability. The degree of marketization of overseas electricity prices is higher, and the residential and non-residential electricity prices in Germany/the United States/Japan and other countries are far higher than those in China. The marketization of electricity price ensures the profit space of downstream operators. The overseas owners are characterized by focusing on performance and reducing costs, so they can give suppliers a higher premium.

Overseas customers have a high recognition of the companies that have introduced the supplier system. Take Kelu Electronics as an example to introduce overseas customers through nearly 2 years of sample delivery. Although Kelu Electronics has been under great pressure of operation and cash flow in recent years, overseas customers are still willing to continue to import orders, and the company's energy storage revenue has continued to exist and its profitability is at a high level in the industry.

2、 Channels

The integration link is directly responsible for the safety, and the safety control ability is the most important. The integration vendor is the primary responsible person for security issues. The safety core of the energy storage system integration is the battery test (DC side), which is characterized by intensive energy, flexible topology, large number of cells and inconsistent characteristics, and is prone to safety accidents. In 2018 and 2019, there were 16 and 11 energy storage accidents in South Korea, causing downstream owners to worry about their safety, resulting in a decline in the growth rate of installed energy storage in 2019. In Beijing's "416" energy storage fire liability determination, the integration manufacturer bears an important responsibility. Therefore, in the context of frequent safety accidents, the safety control ability of the energy storage integration manufacturer for the project is a key concern of the downstream owners.

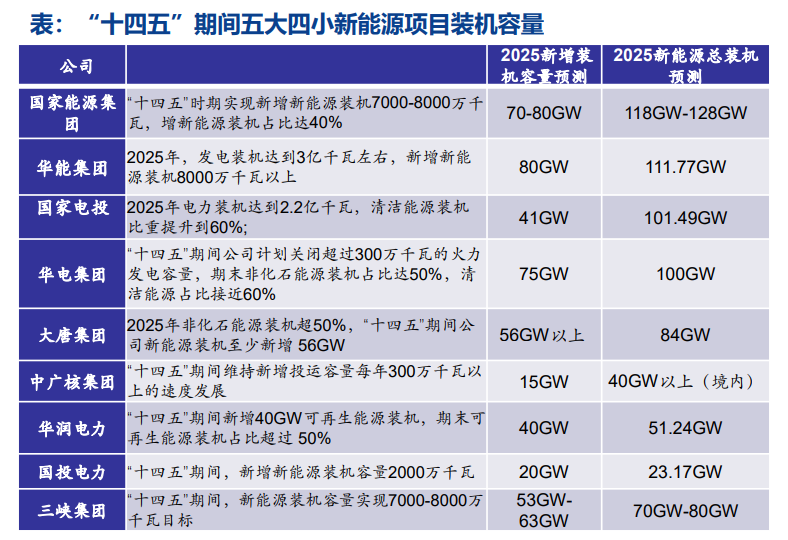

In the field of energy storage, the customer resources are relatively fixed, and the downstream large power central state-owned enterprises have a large voice. With the concentration of downstream customers, the brand advantage will become increasingly prominent. During the 14th Five-Year Plan period in China, most of the new energy projects are constructed by the five major and four small power central state-owned enterprises, and most of the energy storage projects are also constructed by their supporting bidding. They are superimposed on the South China Grid and the State Grid, and the downstream owners of the large storage projects are relatively fixed.

According to the announced installation plan of the five big and four small power generation groups, the total new installed capacity of the five big and four small power generation groups will reach 450GW in 2025. The total installed capacity of new energy in 2025 is predicted to be 689GW. By 2025, the five major and four small power generation groups will undertake more than 50% of the construction tasks of new energy projects. Enterprises that have established long-term cooperative relations are expected to stand out.

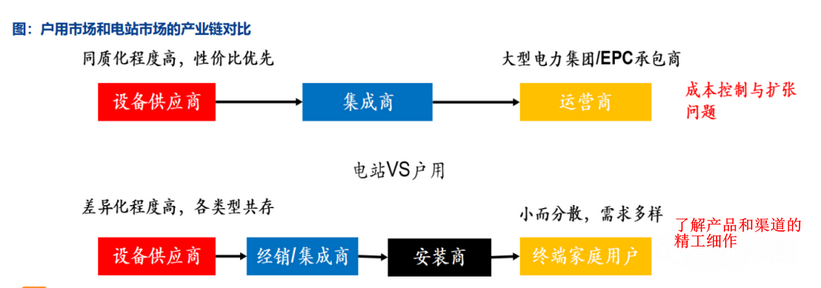

The energy storage project is a business of "old customers", and its reputation is important. Large storage: in the large power station market, the products are homogeneous, and the downstream customers are large power groups or contractors. The key competitive elements of the business model are cost control and scale expansion. The scale advantage of the leading manufacturers is prominent, and the pattern will be further concentrated.

Household storage: Compared with the homogenization competition centered on scale and cost in the power station market, the competition barrier in the household market is mainly reflected in the long-term intensive cultivation of products and channels, and its competition pattern will show a trend of blooming flowers in a long time.

3、 Funds

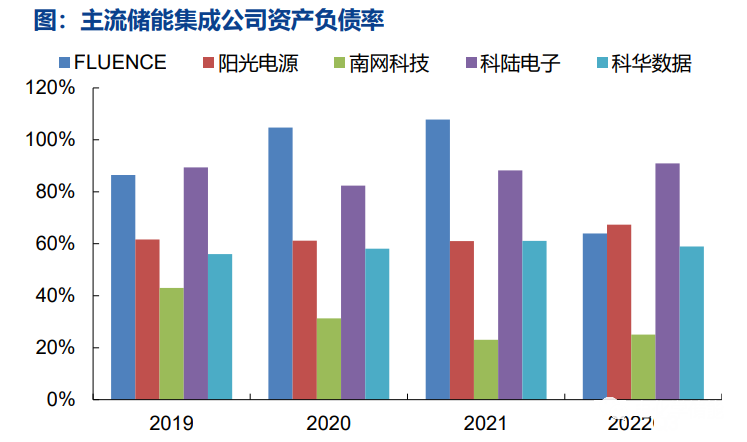

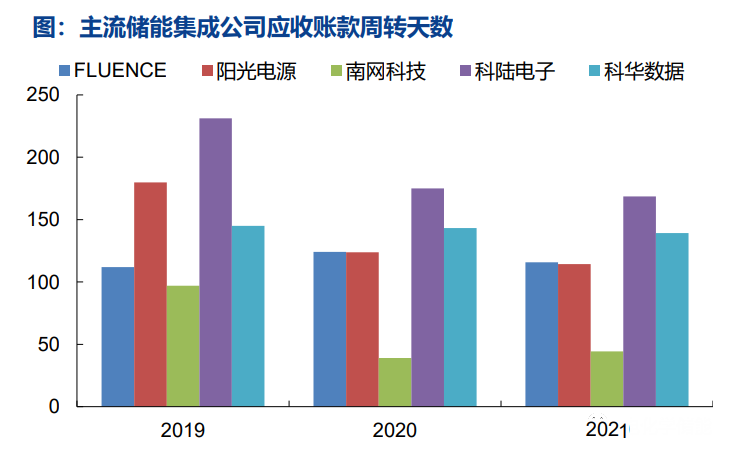

The construction period of large reserves is long, the proportion of funds occupied is high, and the requirements for capital strength are high. The asset-liability ratio and the turnover days of accounts receivable of mainstream energy storage integration enterprises are high, reflecting that they are asset-heavy industries and have a high proportion of capital. At present, the scale of single energy storage projects usually exceeds 100 MW, and the total investment of corresponding projects exceeds 100 million yuan.

The process of large storage construction includes site selection, survey, design, scheme determination, equipment procurement, installation and commissioning, performance test, etc. The construction period is 6-12 months. Most of the downstream owners are central state-owned power enterprises such as the State Grid or the five big and four small power enterprises, which have strong bargaining power and slow payment cycle, resulting in low capital turnover efficiency of energy storage integrators and high requirements for the ability of enterprises to advance funds.

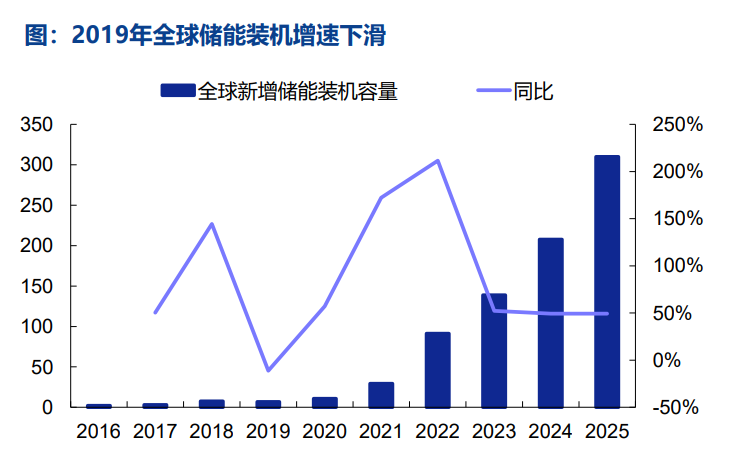

In 2022, the soaring price of silicon materials led to the postponement of some photovoltaic installation projects, and the high lithium carbonate price led to the high price of lithium batteries, which made the owner's enthusiasm for energy storage and grid connection projects low. However, in 2022, the global installed capacity of energy storage and grid connection will still double. In 2023, the cost of photovoltaic modules and the price of lithium carbonate will both decline, which is expected to promote the implementation of energy storage projects. It is an excellent opportunity for energy storage system integrators. |