| The key of new energy is energy storage, and the core of energy storage is " |

| Release time:2023-02-27 10:44:36| Viewed: |

Looking at the moment, new energy+energy storage has been widely recognized, but the market is still accustomed to taking photovoltaic, wind power and other new energy as the protagonist, while energy storage is only a supporting role.

There is no doubt that the new energy industry is prosperous and promising. However, with the rapid growth of wind power, photovoltaic and other installed capacity, the problem of new energy consumption has become increasingly prominent, and the energy transformation is facing serious challenges. Based on this, we increasingly see the importance and urgency of developing large-scale energy storage.

01 Large-scale energy storage becomes the optimal solution - save wind and light

1. The development of new energy is overwhelming. Who can solve the urgent need?

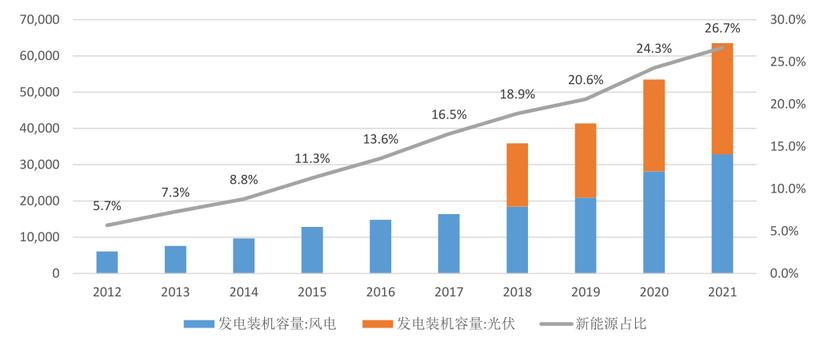

Over the past decade, China's energy transformation has made remarkable achievements in the world. According to the data of the National Energy Administration, by 2021, China's cumulative installed capacity of wind and solar power accounted for 26.7%, and the proportion of wind and solar power generation accounted for 11.7%. Looking forward to the future, the proportion of new energy power generation will continue to increase until it becomes the main power source, while traditional thermal power will gradually fall into the second line, and its ultimate role is as peak shaving and supplementary capacity.

However, in the process of role exchange between new and old energy, the consumption of new energy has become the main obstacle to its continued development.

Figure 1: The installed penetration rate of new energy in 2021 reached 26.7% (unit: 10000 kW) As we all know, wind power and photovoltaic are intermittent energy sources, vulnerable to the impact of climate and weather, and are typical "depend on the weather". In case of extreme weather, the uncertainty of new energy output will easily lead to power shortage in local time.

Whether it is the nationwide large-scale power rationing in 2021 or the staggered peak power consumption in the summer of 2022, the problem of power shortage has seriously affected economic development and residents' lives. The essence behind it is that in the process of replacing traditional energy with new energy, there are problems in the grid connection and consumption of new energy.

On the other hand, the peak output of photovoltaic and wind power is often inconsistent with the demand for electricity. As more new energy is connected to the grid, it will bring a greater impact on the power system, and in serious cases, it will lead to the collapse of the grid frequency, resulting in a large-scale blackout.

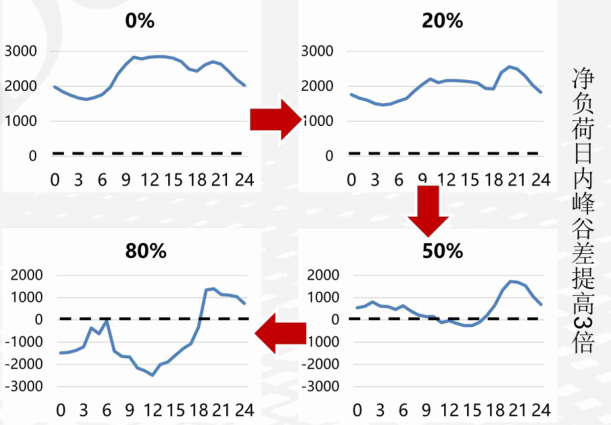

According to the research data of the Global Energy Internet Development Cooperation Organization, when the penetration rate of new energy increases from 20% to 20%, the fluctuation range of the net load of the power system will increase sharply, which will challenge the security of the power grid. Take Shanxi Province as an example. As a major province of new energy installation, the frequency of primary frequency modulation of thermal power units in Shanxi has risen to hundreds of times per day in recent years.

Figure 2: Net load fluctuation of power grid increases with the increase of new energy penetration

So how to solve this problem? Actually, we all know it now, that is, supporting energy storage.

First of all, the allocation of energy storage at the power generation side of new energy can balance the randomness and volatility of new energy, so as to effectively avoid power failure caused by insufficient power generation capacity when the output of new energy decreases or the power load increases. For example, the integration project of scenery and storage.

Secondly, the allocation of energy storage on the power grid is equivalent to adding a "buffer", which can effectively ensure the dynamic balance between the power generation end and the power consumption end.

Finally, as the proportion of traditional adjustable power such as thermal power continues to decrease, it is necessary to introduce energy storage as a new source of regulating capacity to strengthen the flexibility of the power system.

However, at present, the installed speed of energy storage is still far behind the development speed of renewable energy, and there is still an obvious gap. Moreover, we are in the era of deepening electrification, and the future electrification scenarios will be more and more abundant. According to the prediction of the Global Energy Internet Development Cooperation Organization, by 2060, the proportion of electric energy in terminal energy consumption is expected to reach 66%.

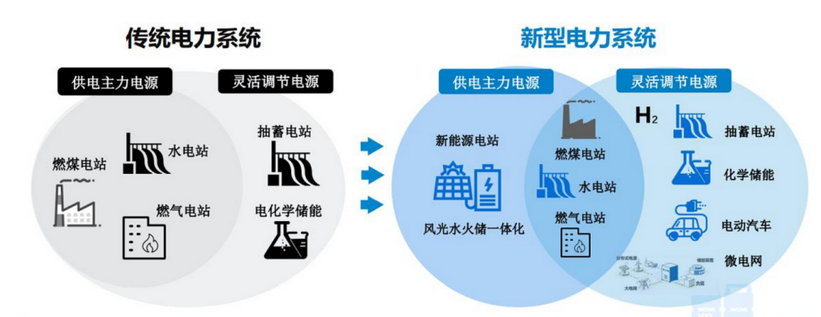

In a word, with the increasing share of photovoltaic and wind power, energy storage is not only an important prerequisite for the development of new energy, but also will deeply participate in the energy transformation process and become a key component of the power system.

Figure 3: Energy storage becomes an important part of the new power system 2. Why large energy storage?

According to the "Fourteenth Five-Year Plan" for Renewable Energy Development, by 2030, China's total installed capacity of wind power and photovoltaic will reach more than 1.2 billion kilowatts. In the face of such large-scale access to new energy, it is conceivable that the power system needs large-scale energy storage to solve the problem of new energy consumption, so as to improve the security and stability of the power system and energy system.

What is large-scale energy storage? As the name implies, it refers to energy storage with large power and capacity. According to the national standard Code for Design of Electrochemical Energy Storage Power Station, large energy storage power stations are defined as energy storage power stations with power of 30MW and capacity of 30MWh and above.

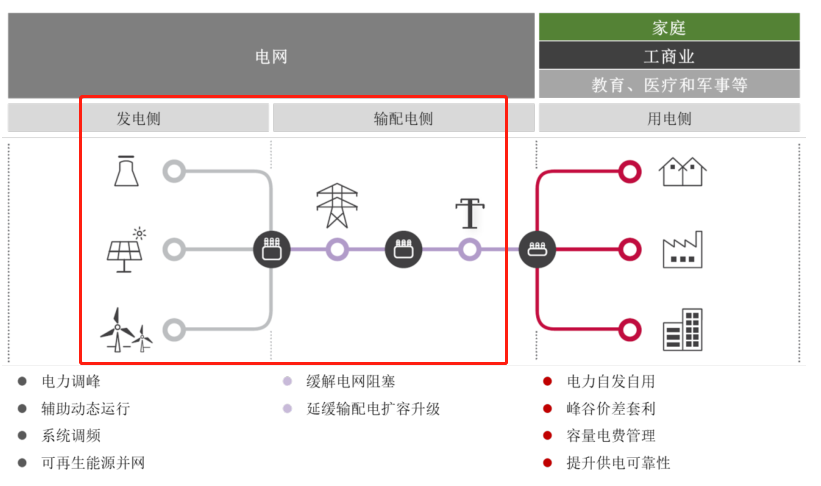

The main application scenarios of energy storage include power generation side (wind farm, photovoltaic power station, traditional power station, etc.), power grid side (power grid company, etc.) and power consumption side (household, industrial and commercial, etc.). Large-scale energy storage is more applied to the power generation side and power grid side.

Figure 4: Application scenario classification of energy storage in power system

At present, the large-scale energy storage routes show a multi-point flowering situation, of which the most concerned are pumped energy storage and electrochemical energy storage.

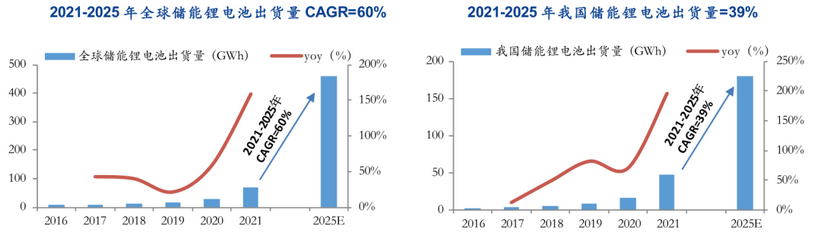

●Pumped energy storage. As the most mature energy storage technology with the largest installed capacity in the world, it accounts for about 86% of China's installed energy storage capacity. It can be said that pumped-storage energy acts as the anchor of the energy system. ●Lithium battery energy storage. With the characteristics of short construction period, flexible location and excellent regulation performance, lithium battery energy storage has become the pioneer of electrochemical energy storage. According to InfoLink data, the global shipments of lithium batteries for energy storage totaled 142.7GWh in 2022, with a year-on-year increase of 204.3%.

●Sodium ion energy storage. Although the energy density of sodium ion battery is not high enough to be compared with lithium battery, it is more economical and safe, and is expected to be widely used in energy storage and other fields in the future, and become an important branch of electrochemical energy storage. At present, companies such as Zhongke Haina and Ningde Times are actively promoting the industrialization of sodium ion batteries.

● All-vanadium liquid-flow battery for energy storage. With the characteristics of high safety, strong capacity expansion, long cycle life and low life cycle cost, it is expected to occupy a place in the field of long-term energy storage in the future.

In general, the diversity of energy storage application scenarios determines the diversified development of energy storage technologies. Various large energy storage technologies complement each other and give play to their unique performance advantages.

02 Large-scale energy storage opens a new situation 1. Growth of volume

In the past, because the penetration of new energy is at a low level, the power system makes full use of the regulating capacity of hydropower, and the flexibility transformation of some thermal power units can meet the requirements of stable operation, so the demand for large energy storage at the power generation end is not urgent.

At the same time, large-scale energy storage is a new link for the power system. In addition, it has a huge scale and high investment cost, but its income is very limited, which has become a cost burden. For a long time, large-scale energy storage for new energy allocation lacked economic driving force, and even there was the phenomenon of idle energy storage and grid connection projects.

Now, in the context of the doubling of the pressure of new energy consumption, the requirements of new energy allocation and storage have been clarified in various places since 2021. Up to now, more than 20 provincial administrative regions in China have defined the proportion and duration of energy storage allocated for new energy power generation projects, and the development of large-scale energy storage has become the consensus of the industry.

In July 2021, the National Energy Administration and the National Development and Reform Commission jointly issued the Notice on Encouraging Renewable Energy Power Generation Enterprises to Build or Purchase Peak shaving Capacity to Increase the Scale of Grid Connection, which again determined the important role of energy storage in the field of new energy at the national level.

2. Improvement of business profit model

Beyond the macro perspective, we will look at the changing trend of large-scale energy storage from the perspective of business operation.

Large energy storage is just needed by new energy power generation enterprises, and its construction cost and profitability have been the focus of the latter. However, most of the energy storage projects that have been built in the past have not yet formed a stable and reasonable income model, and the high construction cost and low income do not match at all.

Until recent years, the profitability of large domestic energy storage projects has been gradually improved through demonstration and exploration in various ways and the introduction of energy storage industry incentive policies.

From the perspective of energy storage revenue, energy storage projects mainly charge at low electricity prices and discharge at high electricity prices to earn the corresponding income. In July 2021, the National Development and Reform Commission issued the Notice on Further Improving the Time-of-use Tariff Mechanism, specifying that the price difference between peak and valley electricity prices should be reasonably widened. In principle, the price difference between peak and valley electricity prices should not be less than 4:1 in places where the system peak and valley difference rate exceeds 40%, and not less than 3:1 in other places.

Especially in recent months, many provinces and cities such as Shanghai, Hubei, Henan, Jiangxi and Shandong have launched a new round of peak-valley time-of-use electricity price mechanism adjustment, with a higher fluctuation ratio of peak and valley electricity prices. As the price difference between peak and valley increases, the profit dilemma of energy storage is expected to be eased to some extent.

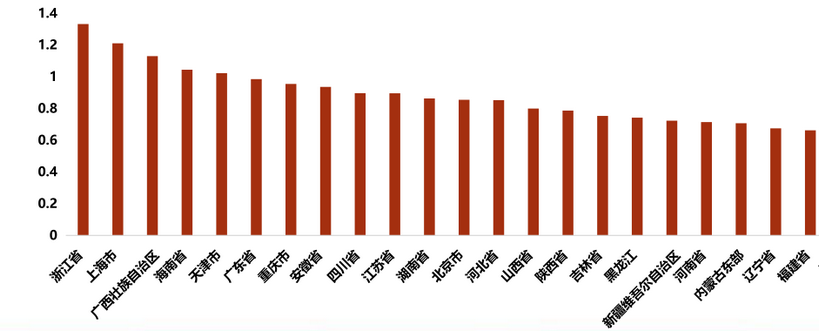

Figure 5: Maximum peak-valley electricity price difference in some provinces in China in October 2022 (yuan/kWh)

Secondly, the market mechanism of electric power auxiliary services has been continuously improved, and the revenue sources of large energy storage have become more abundant, such as the provision of auxiliary services revenue, capacity leasing, capacity compensation, etc. This means that in the past, the problem of a single source of income from large-scale energy storage ushered in room for improvement. In the future, we can make money by doing more "sideline".

For example, China is actively exploring the "shared energy storage" mode to increase the revenue sources of energy storage power stations. Since 2021, Ningxia, Qinghai, Shandong and other provinces have clearly put forward the construction and development of shared energy storage in their policies, and formulated detailed lease price guidance. For example, the "Implementation Plan for New Energy Storage in Henan Province during the 14th Five-Year Plan" issued by Henan Province stipulates that the guiding price of energy storage lease is 200 yuan/kWh/year.

The so-called shared energy storage is to integrate the energy storage resources on the independent and decentralized power supply side and grid side, and submit them to the grid for unified coordination to provide services for multiple new energy power stations, so as to improve the utilization rate and profitability of energy storage resources.

For new energy enterprises, they can enjoy the power to charge and discharge energy storage within the service period to meet their own consumption needs, without the need to build separate energy storage power stations, thus significantly reducing the initial capital investment. For the investors of shared energy storage, after the completion of the energy storage project, the capacity lease fee becomes a stable source of income. At the same time, shared energy storage can also participate in auxiliary power services to obtain auxiliary service fees such as peak shaving and frequency modulation.

Of course, in the face of the objective reality, the development of China's energy storage market is relatively late, and it is undeniable that it is still in the early stage of commercialization. The economy of energy allocation and storage has not been fully developed, and the future commercial profit model needs to be further improved.

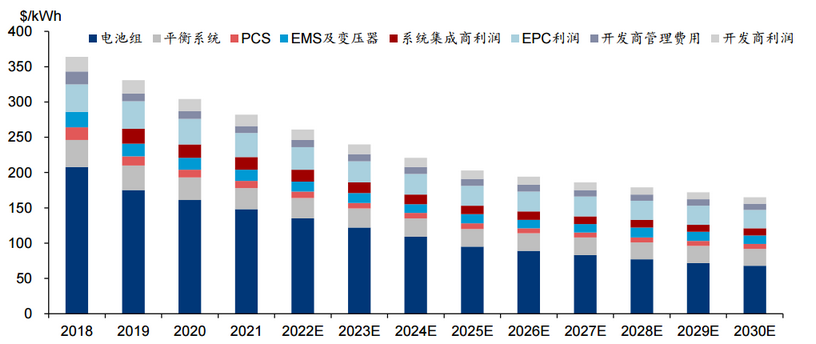

From the perspective of energy storage cost, according to BNEF data, the average price of lithium battery pack dropped from 1100 US dollars/kWh to 137 US dollars/kWh from 2010 to 2020, a decrease of 89%. Next, the core driving force of lithium battery energy storage system depends on the cost to further explore.

On January 29, 2022, the National Development and Reform Commission and the Energy Administration issued the Implementation Plan for the Development of New Energy Storage during the "Fourteenth Five-Year Plan", which proposed the development goal of reducing the cost of electrochemical energy storage system by more than 30% by 2025, to further meet the demand for building new power systems.

Figure 6: The cost of electrochemical energy storage system continues to decline

In fact, the reduction of energy storage cost is crucial to promote the development of new energy. Only if the cost of energy storage continues to decline, can the cost of comprehensive electricity use of new energy continue to decrease, thus replacing the traditional thermal power and successfully realizing the energy transformation.

As early as 2011, Ningde era laid out the energy storage field, but it has been stagnant for many years. It was not until the last two years that the energy storage business of Ningde Times really started to drive on the fast track and became the second largest business of the company. The main reason behind this is that the cost of lithium batteries was too high, which seriously restricted the growth of the installed capacity of lithium batteries.

However, due to the high price of lithium, nickel and other battery raw materials, the value of lithium battery energy storage system cannot be fully released, which largely limits the rapid expansion of its installed capacity. In the future, with the decline of core raw material prices, lithium battery prices will return to a reasonable price range, which will further promote the construction process of lithium battery energy storage projects.

In a word, only when large energy storage projects have obtained reasonable profitability can they promote the expansion of energy storage capacity, and then feed back the large-scale growth of new energy.

3. Future market space calculation

First of all, look at large-scale pumped storage (storage). According to the plan of the National Energy Administration, the installed capacity of pumped storage in China will reach 62 million kilowatts and 120 million kilowatts respectively by 2025 and 2030. If the cost of 6000 yuan/kw is calculated, the total investment in the pumped storage industry will reach 1.6 trillion yuan by 2030, with an average annual investment of more than 160 billion yuan.

Figure 7: Prediction of installed capacity of pumped storage (10000 kW)

In terms of lithium battery energy storage, according to the data of lithium battery in Gaogong, it is estimated that the global lithium battery energy storage shipment will reach 460GWh in 2025, corresponding to the CAGR of 60% in 2021-2025. Among them, China, the United States and Europe are the main markets for lithium battery energy storage.

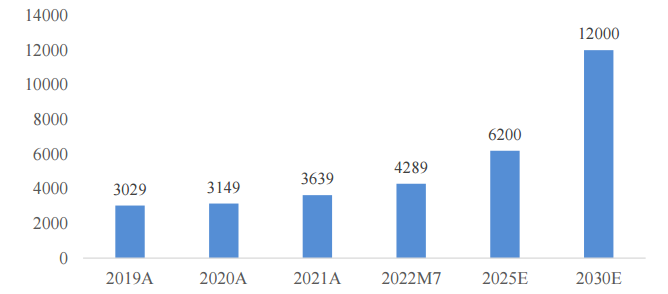

Figure 8: Forecast of lithium battery shipments in 2025 4. Which links will be more profitable?

Looking forward to the future, the installed capacity of new energy will still maintain the trend of rapid growth, and the supporting large-scale energy storage will usher in a deterministic growth, in which the core links of the industrial chain will take the lead in benefiting from the industry growth dividend.

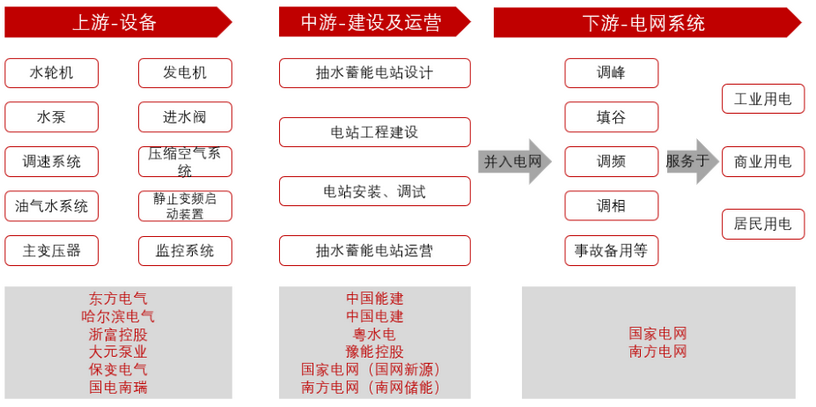

Upstream of the pumped storage industry chain are mainly equipment manufacturers, including core equipment manufacturers such as pump turbines, generators and main transformers. The main suppliers of hydraulic turbines are Dongfang Electric, Harbin Electric, Zhefu Holding, etc; The main suppliers of water pumps are Lingxiao Pump, Dayuan Pump, etc; The main suppliers of transformers are Baobian Electric, Xinhuadu, etc.

The middle reaches of the pumped storage industry chain are mainly power station design and construction and power station operation companies. The main power station design and construction enterprises are China Power Construction Corporation and China Energy Construction Corporation. The power station operation mainly includes the State Grid and China Southern Power Grid.

Figure 9: Overview of pumped storage industry chain

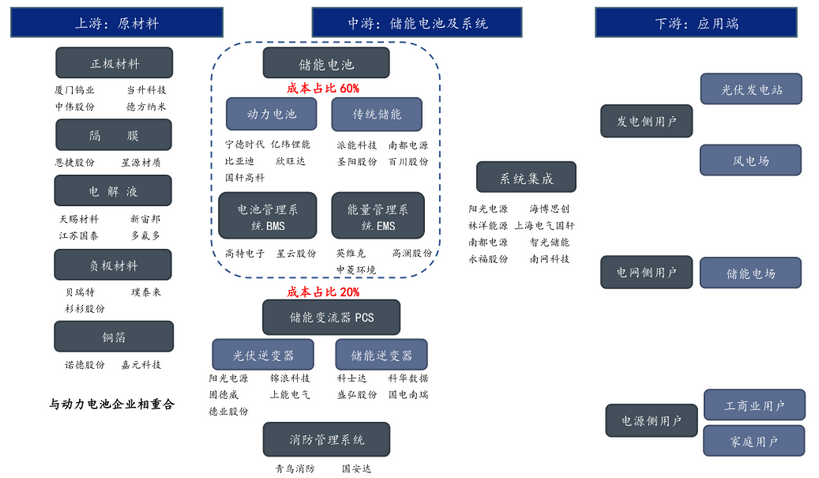

For the lithium battery energy storage industry chain, the core link of energy storage system is composed of energy storage battery, energy storage converter (PCS), battery management system (BMS) and energy management system (EMS). Among them, the energy storage battery is the most important and the most expensive part of the energy storage system, accounting for 60% of the value of the energy storage system, and the remaining costs of PCS, EMS and BMS are decreasing in order, about 20%, 10% and 5% respectively.

Since the technical principles of energy storage battery and power battery are consistent, and the capacity can be switched, power battery enterprises represented by Ningde Times, Yiwei Lithium Energy, Guoxuan Hi-Tech and China Innovation Airlines have taken the lead in entering the energy storage circuit. Up to now, the energy storage products of Ningde Times have covered the power generation side, the grid side and the user side, covering solar and wind power generation energy storage facilities, industrial enterprise energy storage, commercial buildings and other fields; Yiwei Lithium plans to achieve energy storage capacity of 100GWh by 2025.

It is worth noting that the power battery capacity has expanded on a large scale, and then there is the possibility of overcapacity, and the industry competition has become white-hot. Although energy storage battery has lower requirements for energy density than power battery, it has higher requirements for service life, charging and discharging times, battery safety and economy. In the future, battery enterprises with core technology and cost control capability are expected to take the lead.

Then look at the supplier of energy storage inverter (PCS). Because the technical principles and consistency of energy storage inverter and photovoltaic inverter are the same, the manufacturing line can also be flexibly switched, and the competitive pattern of energy storage inverter has some overlap with the photovoltaic inverter industry. PV inverter manufacturers such as Sungrow Power, Shangneng Electric and Jinlang Technology have become important players in the energy storage industry.

Figure 10: Overview of lithium battery energy storage industry chain

|