| Depth! Avoid the "double loss" situation of new energy and energy stor |

| Release time:2023-02-27 11:28:25| Viewed: |

Under the "double carbon" strategy, the large-scale development of energy storage has a strong logic, but in recent years, the problems of the energy storage business model have always troubled its development. Behind the data boom is the general anxiety of the industry. Compared with the two-way efforts of the United States and the European Union at both ends of the policy and the market, China's new energy distribution and storage model currently brings about a "double loss" situation! Only with policy support and market orientation can we achieve high-quality development of new energy storage and promote "win-win" of new energy and energy storage.

1、 Mystery of installed data of energy storage

(1) Official and industrial caliber of energy storage installation

On February 13, the Energy Administration held a regular press conference in Beijing to release the development of renewable energy in 2022. The data showed that new breakthroughs were achieved in new energy and energy storage in 2022. In terms of energy storage, 8.7GW of new energy storage projects were put into operation nationwide at the end of 2022 (of which electrochemical energy storage accounted for about 98%), with an average energy storage time of 2.1 hours, an increase of more than 110% over the end of 2021. This is the first time that the Energy Administration has officially released data on energy storage.

At the initial stage of China's energy storage development, due to its diverse application scenarios and complex technical routes, most of the energy storage projects are not standardized and large-scale, and few are included in the scheduling operation. There are great difficulties in data statistics. The Zhongguancun Energy Storage Alliance and other industry organizations release the white paper and other reports on energy storage development every year to publish the energy storage installation data, so that we can see the process of energy storage development.

With the positioning of energy storage as an important infrastructure for the construction of new power systems, the energy authorities began to pay attention to the real development of energy storage. In April 2022, the Cost Investigation Center of the National Development and Reform Commission published an article on the official website titled "Improving the Energy Storage Cost Compensation Mechanism and Helping to Build a New Power System with New Energy as the Main Body", which mentioned for the first time that the cumulative installed capacity of electrochemical energy storage by the end of 2021 would exceed 4 million kilowatts, and then used this data in the officially mentioned energy storage installations.

(2) Differentiate and analyze the real situation of energy storage and installation

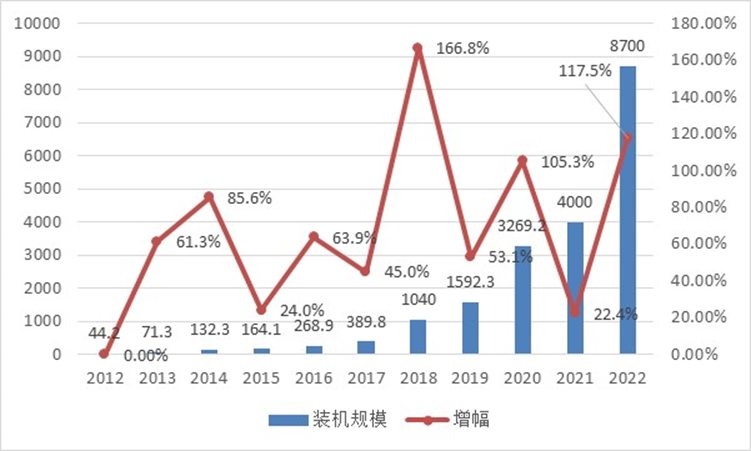

Accumulated installed capacity of energy storage over the years (official data will be used in 2021 and 2022)

Since no public data was officially released before 2021, the data released by the Zhongguancun Energy Storage Alliance was used in this article from 2012 to 2020. On the whole, energy storage has entered a rapid development stage since 2017. However, due to the use of official data in 2021, the new installed capacity in 2021 is less than 1GW, which may be due to the mismatch between the industrial statistics and the official statistics.

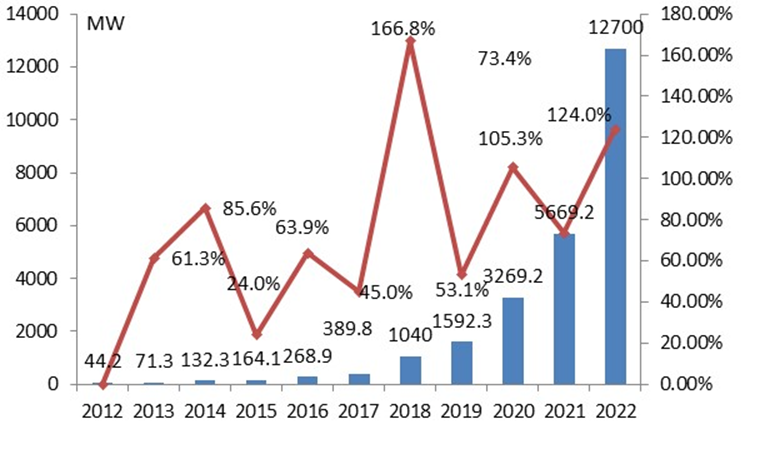

According to the data of Zhongguancun Energy Storage Alliance, by the end of 2021, the total installed capacity of energy storage will be about 5.7GW (40% higher than the official data), and 2.4GW/4.9GWh will be added that year. However, the industry data initially disclosed in 2022 was 12.7GW of total installed capacity, and 6.9 GW was newly added that year, still more than 40% higher than the official data.

Accumulated installed capacity of energy storage over the years (industry data)

If only the installed capacity data of 2021 and 2022 are not enough to stimulate the enthusiasm of all sectors for energy storage, in fact, the domestic expectation for the prosperity of the energy storage industry lies in the guidance of bidding data. In 2021, the total bidding capacity of domestic large energy storage EPC and equipment will reach 10.1GWh, more than twice the total new installed capacity of the year (industry data); The bidding capacity of the energy storage project in 2022 is about 44GWh, 3-4 times of the new installed capacity in that year. The "early prosperity" of the installed capacity data of the energy storage industry can only be explained by "bidding this year and putting into production next year". According to this calculation, the installed capacity of energy storage in China will reach more than 40GWh in 2023, and nearly half of them will be shared energy storage. The explosive period of energy storage seems to be coming soon!

2、 Why is new energy+energy storage moving towards "double transmission"?

However, the rapid development of energy storage in China is not unique, and its development situation is by no means flat.

The energy storage of the United States and the European Union has also entered a growth period, which is not too much for China. Benefiting from the support of the US Inflation Reduction Act, the capacity purchase of power grid companies and the market mechanism, the increase of new energy storage in the United States will exceed 10 GWh in 2021, 13-15 GWh in 2022 and nearly 30 GWh in 2030, with a growth rate that is more than that of China. Driven by high electricity prices, the EU's "new energy+energy storage" power supply mode has economic advantages, and the EU's new energy storage will also reach 3.5GWh in 2021.

Compared with the relatively clear development logic of the United States and the European Union, China's energy storage development has always been hampered by the unsound business model. In theory, new energy storage, as an important regulation facility of the power system, has a direct role in improving the absorption capacity of new energy. The development model of new energy+energy storage should effectively achieve the "win-win" between the two, but the actual situation in China is far from that!

1. The allocation of energy storage increases the cost burden of new energy

Based on the idea of "who solves the problem", requiring new energy to allocate energy storage in proportion has become the main reason for promoting energy storage growth in recent years, but allocating energy storage has significantly increased the cost of new energy development. According to a simple calculation, the photovoltaic project will increase the cost of electricity consumption by about 0.6-0.7 cents per kilowatt hour if the energy storage is configured according to 10% of the installed capacity and 2 hours, while many provinces require a higher allocation ratio.

For new energy, the allocation of energy storage is "the larger the scale, the greater the harm". From the perspective of improving regulation capacity, compared with the expensive energy storage, if new energy has more freedom to purchase flexible resources such as demand response, deep regulation of coal and electricity, or adopt its own power management behavior, its cost pressure may be less.

2. Forced allocation of energy storage cannot guarantee the high-quality development of energy storage

The policy of allocating energy storage in proportion only takes new energy storage as the threshold for new energy grid connection, and does not establish a supervision and assessment system for its operation effect, which makes the energy storage effect inadequate. At the same time, in most provinces, new energy has not yet participated in the electricity market transaction as a market subject, and the after-sheet energy storage of new energy can not gain benefits from participating in the spot market or the auxiliary service market, which further aggravates the "inertia" of the new energy-side energy storage to participate in the operation.

According to the survey report of China Electricity Union, the equivalent utilization coefficient of new energy storage in China is only 12.2%, and the distribution and storage coefficient of new energy is as low as 6.1%. The allocation of energy storage has little effect on improving the absorption capacity of new energy projects. Because there is no monitoring mechanism for actual operation, in order to reduce costs, it is difficult to ensure the engineering quality of the energy storage power station configured with new energy, which is not conducive to the overall improvement of the energy storage industry.

3. Is shared energy storage only the first stick of "beating drums and passing flowers"?

As an independent entity, shared energy storage has been able to participate in the spot market or auxiliary service market transactions. At the same time, it is easier to form scale advantages for independent allocation of energy storage for new energy, and it also alleviates the investment pressure of new energy operators. At the stage when the cost of self-built energy storage is high and the implementation of the policy of allocating energy storage in proportion to new energy is not very rigid, new energy operators take a negative attitude towards self-built energy storage, and the tendency to meet the allocation and storage requirements by leasing and sharing energy storage is more obvious when necessary.

But shared energy storage is also difficult to solve the fundamental problems of business model. At present, the compensation or price standard for participating in peak-shaving auxiliary services is generally 0.2-0.5 yuan/kWh, and the average value of the peak-valley difference of the daily time-of-use electricity price in several pilot spot markets is also generally lower than 0.5 yuan/kWh (about 0.4 yuan/kWh in Shandong). At the same time, considering the factors such as insufficient utilization of energy storage, its market-oriented income still needs to be discounted, so the gap between shared energy storage and recovery costs is far away only by participating in market transactions, Finally, it is still necessary to transfer a large part of the cost to the new energy operators through the lease fee, which does not change the essential logic of the development of energy storage, but the shared energy storage occupies the first position of "beating the drum and passing the flowers". The high rental cost of shared energy storage also leads to the low rental rate, which further leads to the waste of investment costs.

To sum up, unlike the European Union, which mainly relies on market mechanism, the United States relies on policy and market forces in both directions. Although China has constantly created conditions for marketization of energy storage costs, the cost of energy storage development is still mainly borne by new energy. In the case that the cost of new energy and energy storage has not been reduced rapidly, requiring new energy to be bound with energy storage may adversely affect the development of new energy and bring about a situation of "double transmission".

3、 Break the situation and make new energy and energy storage move towards "win-win"

For the current situation of breaking the "bull" in the development of energy storage and new energy, to achieve high-quality development of new energy storage, and to make the two truly move towards a win-win situation, we still need to make efforts from both the policy and the market.

1. Policy

For emerging industries, policy support is crucial, and the development of renewable energy at home and abroad has proved this point. Although China's large-scale financial subsidies are no longer realistic, the role of policy regulation and guidance is crucial. The author believes that there are still many tools available:

(1) Change the "one-size-fits-all" way of allocating and storing energy in proportion to new energy, and make new energy have the power to choose a more economical way to improve its flexible operation ability, and also promote the operation effect of allocated and stored energy, which can really play a role in regulating energy storage. For new energy, it can not only improve consumption but also reduce the regulation cost;

(2) The introduction of investment tax credit policy and the reduction and exemption of value-added tax and income tax on energy storage projects will not only boost the investment enthusiasm of energy storage, but also increase the national financial pressure;

(3) Strengthen the "double carbon" constraint, and improve the relative competitiveness of new energy+energy storage projects, such as implementing the decomposition of non-water renewable energy consumption responsibility weight on the user side, and giving higher completion weight to the new energy generated by energy storage.

2. Market

(1) Establish a more equal and transparent market mechanism to improve the coverage of the regulatory market

The large-scale development of energy storage and the improvement of regulation income, on the one hand, come from the reduction of its own costs, on the other hand, from the fair opening of the regulatory market (including the spot market). In China, the power grid company provides a general basis for system security by means of centralized dispatching, which ensures the stable supply of power in China, but also brings asymmetric information and unfair competition to regulate the market. For example, the capacity procurement mechanism implemented for pumped storage power stations excludes energy storage, which compresses the living space of new energy storage; The management of orderly electricity use also greatly reduces the role of regulating resources. For the market design of regulatory resources, we should reduce unnecessary external intervention and try to improve the coverage of marketization.

(2) Capacity procurement mechanism cannot be absent in the short term

For different regulatory resources, we should not only be fair and equal, but also take into account the differences of various varieties. Energy storage depends entirely on the spot market or auxiliary service market for profit, which can only be realized after the completion of the new power system dominated by new energy. In the scenario of new energy as the main body, the regulation resources of the power grid are very scarce. Intermittent power shortage and intermittent power surplus will alternate. Only when the price difference conditions for energy storage profit are met can they appear, but the balance between economy and power grid reliability still needs to be considered.

At this stage, for the new type of energy storage similar to pumped storage, its one-time investment is large, and the capacity income provides more stable income for energy storage, which is more consistent with the asset characteristics of energy storage, and also reflects the commodity attribute of energy storage to increase the grid capacity adequacy. It is suggested that under the premise of government planning and supervision, increasing the capacity procurement of power grid companies and establishing a competitive capacity market can effectively promote the development of large-scale energy storage and improve the regulation and guarantee capacity of the power system. |