| Charge pile operator turns into "load aggregator" |

| Release time:2023-03-07 09:52:21| Viewed: |

1、 Why is the charging pile operator a natural load aggregator

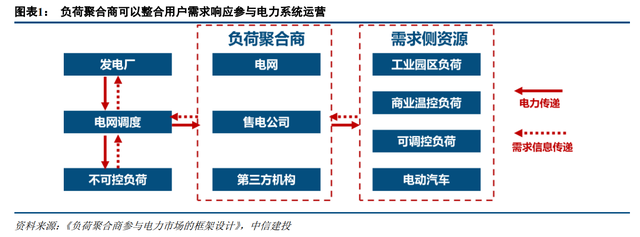

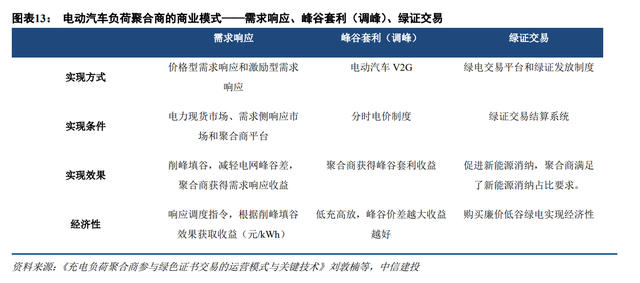

1.1 Typical mode of load aggregator: integrate scattered loads into the power market, provide services and obtain benefits

Load Aggregator (LA) is a new service enterprise registered by power selling companies through demand response management platform under the background of demand response development, and is one of the main participants in demand-side response.

Load aggregators can integrate distributed user demand response resources to participate in power system operation. On the one hand, they can provide opportunities for small and medium-sized load users to participate in market regulation; On the other hand, we can explore the demand response potential of the load through professional technology and provide auxiliary service products required by the market.

Market positioning: load aggregators can be seen as participants in the electricity market (mainly concentrated on the demand side).

Features&advantages: The biggest advantage of load aggregators is that they can integrate a large number of small and medium-sized load users' resources to meet the market regulation standards, and provide the possibility for small and medium-sized load users to participate in the power market. At the same time, load aggregators can guide relatively dispersed small and medium-sized users to participate in demand response through more professional technology and marketing means, and fully explore the demand response potential of load.

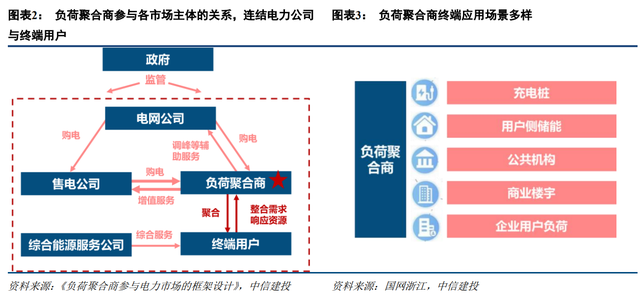

The operator is located in the middle of the charging pile industry chain, connecting with charging pile manufacturers and new energy vehicle enterprises and other customers.

The user demand comes from the charging demand of the significantly growing electric vehicle users. The charging pile operators access the electricity market by integrating the demand of individual users (single charging pile), participate in many activities such as the income from the peak-valley electricity price difference and auxiliary services in the electricity market, and obtain excess income.

二、 How charging station operators participate in demand-side response and auxiliary service market

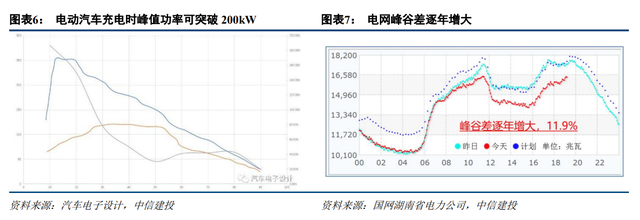

As a kind of electric load, electric vehicle charging will change the shape and characteristics of the load curve when it is superimposed on the original load of the power grid. As shown in the figure, the peak power of DC fast charging can exceed 200kW, which has far exceeded the normal peak power of a household (usually around 10kW).

Because the charging load curve is highly consistent with the residential electricity consumption law (usually the charging period is 7:00-10:00 at night, which is also the peak load period at night), it will significantly increase the peak-valley difference of the grid load, bring great difficulties to the grid power balance and peak shaving balance, and even threaten the security of the grid.

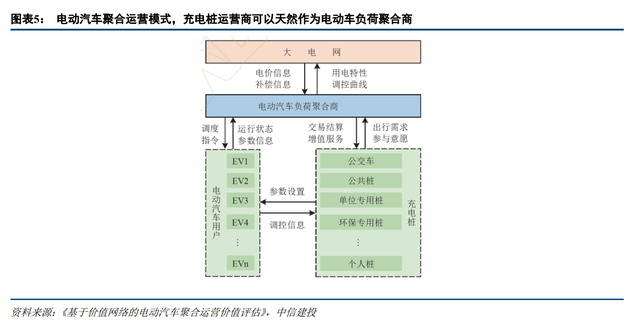

The electric vehicle charging station operator is a natural load aggregator. When the grid is faced with short-term peak shaving and valley filling demand, if the electric vehicle can be concentrated in the charging station for high-power charging and discharging under the condition that the user has the willingness to participate, it can provide the grid with demand response resources in a more time-saving and efficient manner, and can also be used as a supplement when other response resources are insufficient.

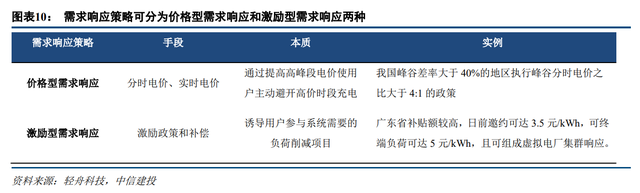

Demand response is widely used by dispatchers to implement guiding scheduling strategies. According to the response rules, there are two scheduling strategies for electric vehicle charging stations (aggregators) to stimulate orderly charging of electric vehicles: price-based demand response and incentive demand response.

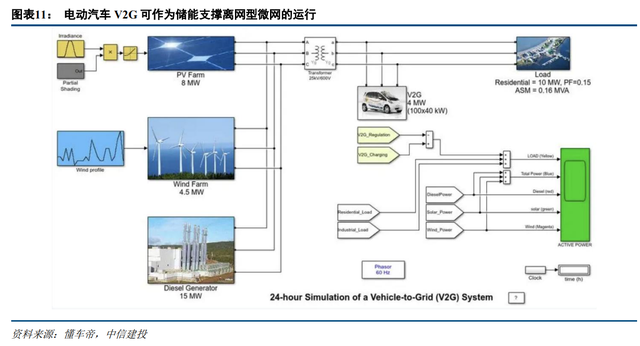

In addition to guiding the charging of electric vehicles, load aggregators (charging station operators) can also guide charged electric vehicles to reverse discharge to the grid to support system power balance.

Electric vehicles under V2G mode are similar to industrial and commercial energy storage, and their economy is realized through peak-valley arbitrage.

However, this process requires aggregators (i.e. electric vehicle charging pile operators) to aggregate their operating charging pile resources (and connected electric vehicles) and connect them to the grid for dispatching.

After the implementation of the spot market, as an electricity market entity, the aggregator can also determine the charging or discharging strategy for the charging pile resources under its control according to the load forecast to maximize revenue.

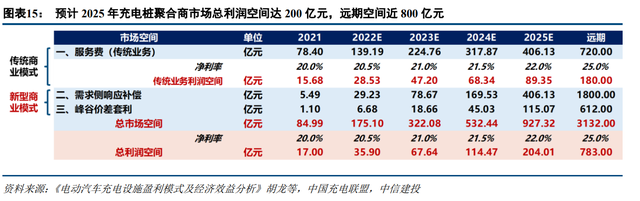

Space measurement: the new business model will contribute nearly half of the revenue in 2025

As a natural load aggregator, in addition to the traditional business model of charging service fees, charging pile operators can also benefit from demand response, peak-valley arbitrage (peak shaving) and other ways. From 2023, with the gradual promotion of various business models, the income from the new business model will become the main source of income for the charging pile aggregator.

It is estimated that the total space of the charging pile aggregator market will reach 92 billion in 2025, and the revenue of the new business model will contribute more than half.

It is estimated that the total profit space of the national charging pile aggregator market will reach 20.4 billion yuan in 2025, and the long-term profit space will reach 78.3 billion yuan.

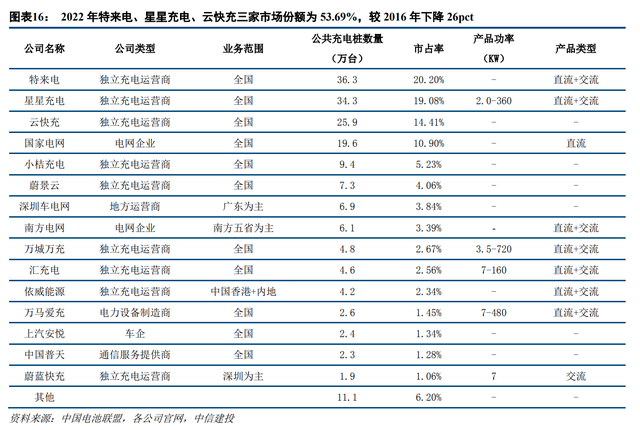

三、 Charging pile operator pattern: grid enterprises take the lead, and third-party independent operators bloom The large-scale laying of charging piles can not be separated from the support of huge funds. The national team represented by the State Grid of China took the lead in completing the construction process of public charging piles from standard to infrastructure to the formation of demonstration sites.

Subsequently, the third-party independent operating companies and automobile companies became the main force of the new pile construction by virtue of refined services and strong user stickiness. Among the CR15 operators, there were as many as 9 third-party independent operating companies.

According to the China Battery Alliance, in 2022, the market share of Telnet, Star Charging and Cloud Fast Charging was 53.69%, down 26 pct from 79.7% in 2016.

State Grid: It is a pioneer in the charging pile industry and is committed to creating an electric vehicle ecosystem.

State Grid is one of the first enterprises to participate in the construction of charging facilities. It established the State Grid Electric Vehicle Service Company in 2015. At present, the company has built more than 2000 expressway fast charging networks with "ten vertical, ten horizontal and two ring" highways as the backbone network.

In addition, the company also launched "e-charge" APP and applet to help users query the location and real-time status of the company's highway charging stations, so as to plan the ideal route in advance.

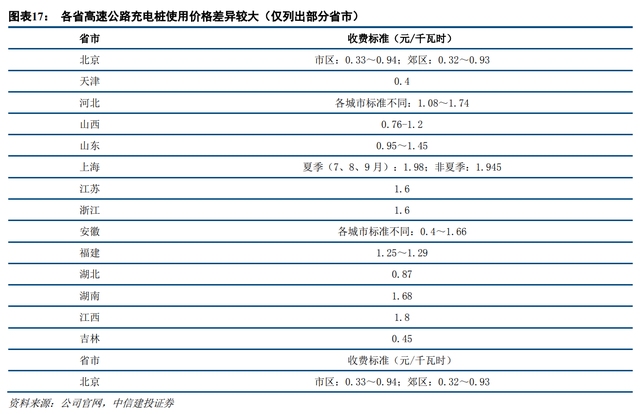

At the price side, the charging pile charges two charges: electricity and service charges. Among them, the electricity charge is subject to the national electricity price policy, and the upper limit of the charging service charge standard is set by the relevant provincial units, so the charging prices vary greatly from province to province.

We call to be the leader of electric vehicle charging pile and enter the virtual power plant.

The company is a holding subsidiary of Qingdao Trude, a manufacturer of box-type electric equipment, and was founded in 2014 with a shareholding ratio of 77.71%. The company is the leader in the charging pile industry, with 363000 public charging piles deployed, accounting for 20.2% of the market.

The company is committed to creating "electric vehicle charging system network".

The construction and operation of the virtual power plant has been actively planned since the special call in 2019, and an announcement was issued in October 2022, proposing to invest 100 million yuan to set up Shanghe Special Call in Qingdao to promote the construction of a virtual power plant ecological and management platform based on the "charging network+microgrid+energy storage network" linked to electric vehicles.

In 2022, the Telnet virtual power plant platform has completed the docking with 16 domestic home appliance network dispatching centers. There are 1885 charging stations participating in peak shaving, with a total peak shaving capacity of 1045.35MW, and the aggregate capacity has been dispatched under different scenarios of more than 300MW.

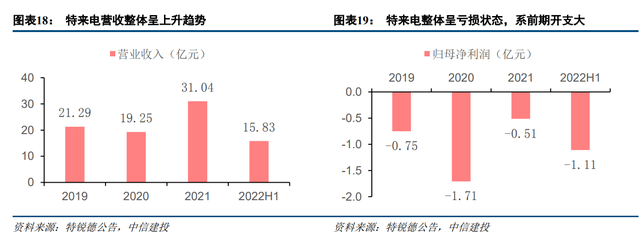

According to the announcement of Trudeaux, the operating revenue of Trudeaux in 2019-2022H1 was 21.29/19.25/3.104/1583 billion yuan respectively, and the year-on-year growth rate of 2020-2021 was -9.58%/61.24% respectively.

However, the company is still in a loss state as a whole, with a loss of 0.75/1.71/0.51/1.1 billion yuan respectively in 2019-2022H1. We judge that there are three main reasons:

1) The gross profit rate of the charging pile industry is about 20%, and the gross profit rate of new energy vehicles, charging business and other businesses of the company in 2020 and 2021 is 21.96% and 22.07% respectively;

2) The company spends a lot on piling, rent, electricity and promotion, which erodes the company's profits;

3) According to relevant reports of the company, in order to achieve the goal of charging network ecosystem, the company has invested up to 2 billion yuan in research and development in the past eight years. At present, the profit generated by the company's charging service is not enough to cover the research and development expenses.

Star charging: relying on the channel resources of the parent company has inherent advantages. In addition to playing the role of platform, the company has rich technical reserves in the field of charging. As of April 2022, the company has more than 900 pieces of intellectual property rights. At the same time, it has independently developed a number of DC and AC charging equipment, with a power coverage of 2.0-360KW.

Langxin Technology: open up the ecosystem of the Internet platform and give full play to the synergy advantage of traffic entry.

The company is a leading enterprise in the informatization of China's energy industry. In 2019, it created the third-party aggregated charging platform "Xindian", and launched the aggregated charging service operation in 2020.

As of 2022H1, the company has reached cooperation with head operators such as Telnet, Star Charging, State Grid, China Southern Power Grid, etc., with a total of more than 500 charging operators, and more than 500000 charging piles in operation, with a year-on-year growth rate of 67% and 150% respectively.

Based on the company's long-term accumulation in the operation of the digital life scene platform, Xindian has built a charging ecosystem with mature Internet service portals such as Alipay, Gaode, WeChat, Baidu, etc., to support users to use Alipay to scan codes and pay fees, effectively improving the utilization rate and awareness of the platform.

Due to the large investment in technology research and development and market expansion of New Power Way, it has not brought corresponding revenue growth to the company in the short term. The operating loss of 22H1 New Power Way has an impact on the company's net profit of about 28 million yuan.

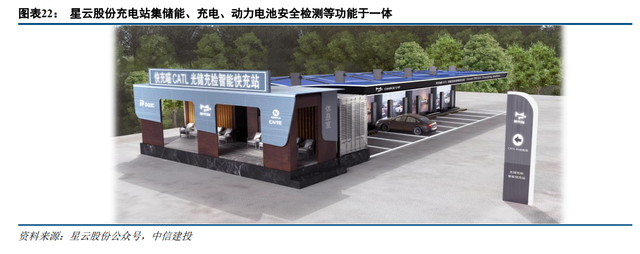

Xingyun Co., Ltd.: The lithium battery industry chain has been extended vertically, and the integrated project of storage, charging and inspection has been launched.

The company is committed to building an industrial chain from "new energy vehicle battery manufacturing to new energy vehicle battery charging service equipment", developing charging piles, operation management platforms and other related products through its holding subsidiary "rechargeable cat energy" and participating companies, and carrying out charging operation services.

With its accumulation in the field of energy storage, the company has developed DC fast charging technology, which can improve the charging efficiency by more than 25% through intelligent control of power output.

In terms of electric pile construction, the company has carried out energy storage strategic cooperation with Time Star Cloud and vehicle charging network, and built "integrated intelligent charging stations for storage, charging and inspection" in Fuzhou, Fujian, Taizhou, Zhejiang, Beijing and other places, integrating energy storage, charging, power battery safety detection and other functions.

In terms of platform construction, the company is one of the first batch of certified pile enterprises in the "State Grid Electric Social Pile Open Platform", relying on the big data energy internet cloud platform, with intelligent scheduling, energy management and other functions.

At present, there are four main profit models for charging piles: electricity and service fees, parking fees, and other income. Among them, electricity and service fees are the main sources of income for electric vehicle charging piles in China. The selling price is generally based on the general industrial and commercial electricity price. The charging service fees are based on the guidance price issued by local governments before 2020, and the market-oriented pricing will be gradually released after 2020. According to the article "Profit Model and Economic Benefit Analysis of Electric Vehicle Charging Facilities", the economy of four charging stations is calculated. The configuration, cost and economy of different charging stations are as follows.

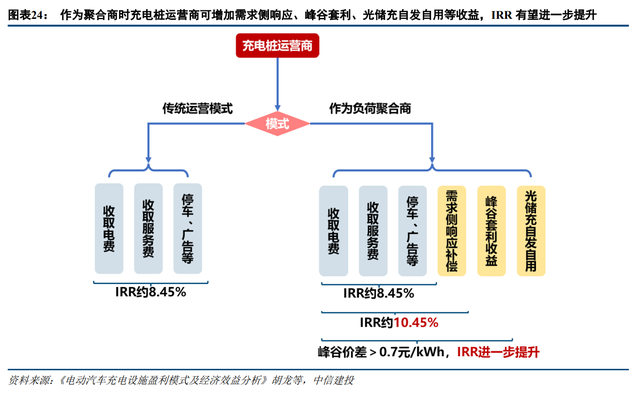

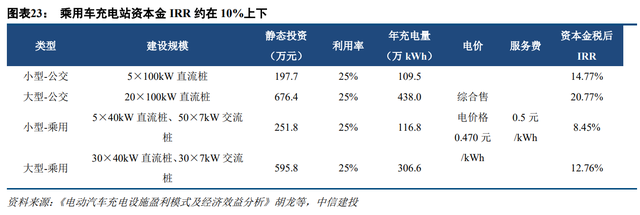

The above calculation only considers the economy of charging stations selling electricity by charging (purchased at the comprehensive selling price) and charging 0.5 yuan/kWh of service fee, and does not consider the additional revenue model when charging stations participate in the demand-side response and other power markets as load aggregators.

If the charging station is considered as a load aggregator to participate in demand-side response, peak-valley arbitrage and other revenue models, the economy is expected to improve. Assuming that 5% of the charging capacity of the charging station participates in demand-side response every year, according to the demand-side response compensation standard of 3.5 yuan/kWh, the charging station for small passenger vehicles in Figure 21 can increase its revenue by about 204400 yuan per year.

For small passenger car charging stations, the capital IRR is 8.45% when they do not participate in the demand-side response, and the IRR will increase by about 2 pct after participating in the demand-side response.

If the income models such as peak-valley arbitrage are superimposed, it is necessary to configure facilities such as battery energy storage. When the peak-valley price difference reaches 0.7 yuan/kWh, peak-valley arbitrage will have a certain economy, and the IRR is expected to be further improved.

With the increasing penetration of new energy vehicles, the demand for charging pile terminals is increasing, and the voice of operators in the middle reaches of the industrial chain is rising. As a natural load aggregator, charging pile operators can make profits through demand response, peak-valley arbitrage (peak shaving), and green card trading to promote new energy consumption and other business models. Its development is imperative.

Industry companies: Langxin Technology (the leader of energy informatization), Lvneng Huichong, Xingyun Co., Ltd., Trude (the subsidiary Telian is the leader of charging pile), etc.

risk analysis

In terms of demand: changes in national infrastructure policies have resulted in less than expected investment in PV and energy storage; Economic growth slowed down, and the growth of industrial and commercial electricity consumption slowed down; Marketization leads to the reduction of peak-valley price difference, etc.

On the supply side: the prices of lithium resources, copper resources, steel and other bulk commodities rose; The supply of IGBT and other power electronic devices is tight, and the localization progress is less than expected; Due to the limitation of installation space, suitable industrial and commercial owners can not install enough.

In terms of policy: the demand-side response to relevant policies is less than expected; The compensation standard of capacity tariff is lower than expected; The progress of electricity spot market is less than expected; The peak-valley price difference of electricity is less than expected; The approval process of fire protection, environmental assessment and energy assessment is too strict.

In the market: the intensified competition has led to lower gross profit margin and profitability of energy storage batteries, integrators and PCS manufacturers than expected; Transportation and other costs rose.

In terms of technology: the cost reduction progress of electrochemical energy storage and other technologies is lower than expected; It is difficult to further improve the reliability of energy storage technology; The cycle efficiency stagnates.

In terms of mechanism: the promotion of electricity market mechanism is less than expected; Supporting services, capacity compensation and peak-valley price difference in the spot market are less than expected; Emerging market mechanisms such as virtual power plants and demand-side management are less than expected.

|